Covering November Market

November was a turbulent month for stocks in which major indexes pulled back sharply before recovering most of their losses.

Concerns that there may be a bubble in the artificial intelligence market, doubts in relation to the timing of US interest rate cuts, and weakness in the crypto markets were some of the main drivers of the volatility.

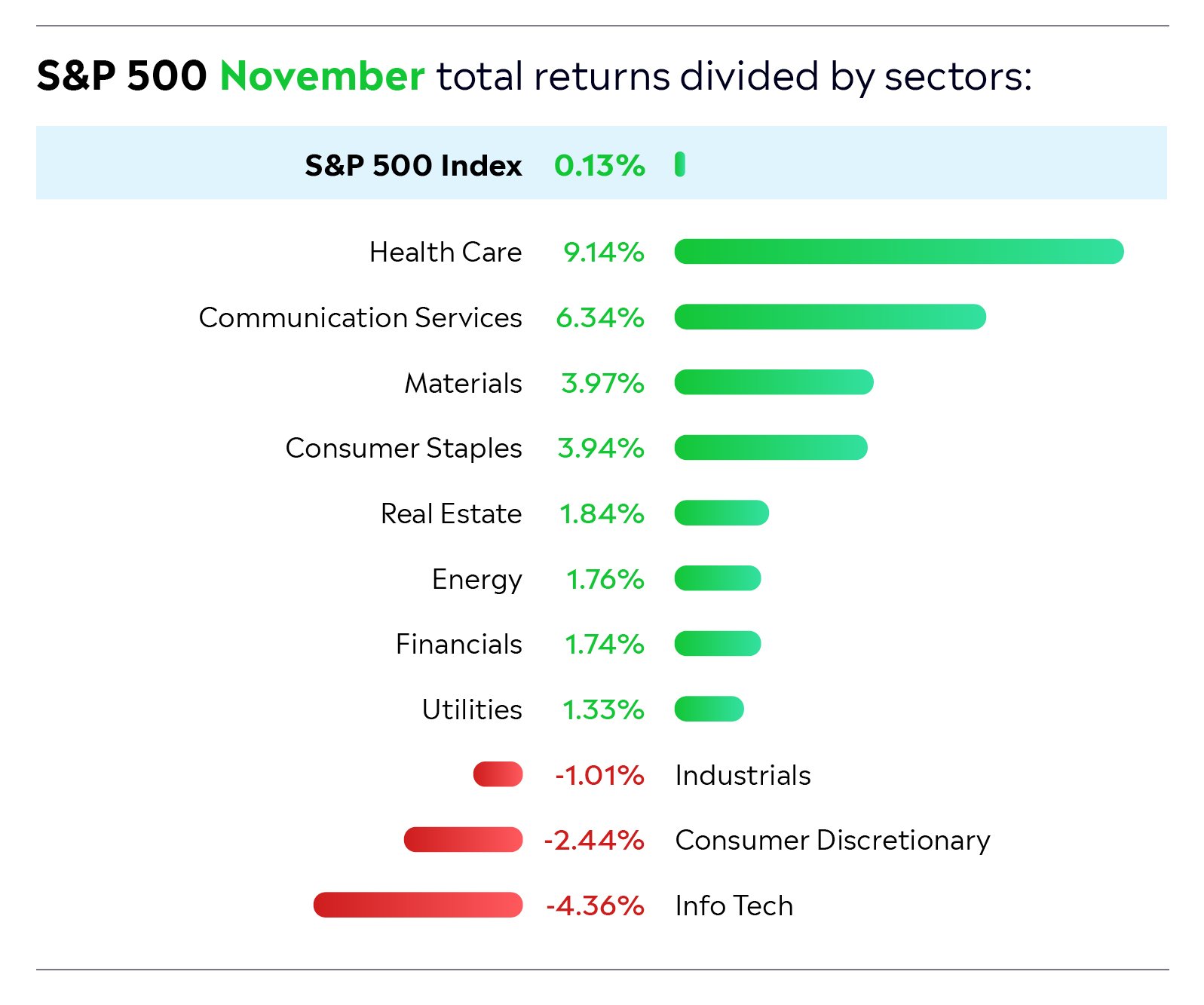

The best-performing sector was Healthcare, which outperformed every other sector by a wide margin. Technology, which saw some profit taking, was the biggest underperformer.

There were many major developments in the AI space in November.

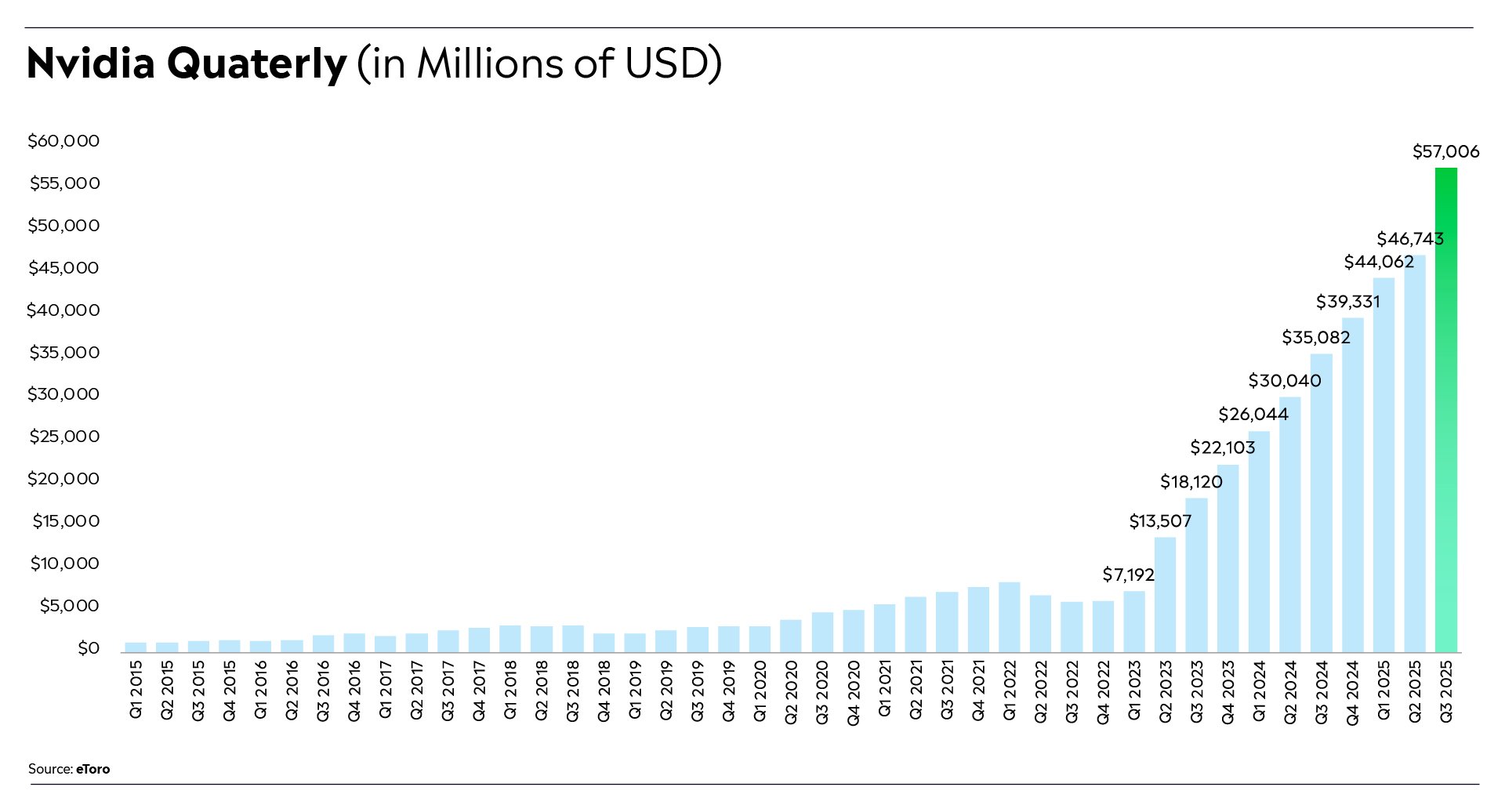

Early in the month, Palantir released its earnings for the third quarter of 2025 and they were very strong, with revenue growth accelerating to 63% from 48% in the previous quarter. This performance was driven by rapid uptake of the company’s AI software by American businesses, with revenue in its US commercial business up more than 100% year on year. AMD then came into focus after a blockbuster presentation at its annual Financial Analyst Day. Here, the company dramatically increased its data centre total addressable market (TAM) forecast, saying that it now believes that the TAM will exceed $1 trillion by 2030, up from a previous estimate of $500 billion by 2028. It also said that it is targeting 60% annual revenue growth in its data centre business over the next three to five years. In the second half of the month, Nvidia produced its Q3 earnings and they were once again spectacular. For the quarter, its revenue was up 62% year on year to $57 billion – an incredible rate of growth given the company’s size. Looking ahead, the company said that it has visibility to half a trillion dollars in Blackwell and Rubin chip revenue from the start of this fiscal year through the end of calendar year 2026.

Despite all this momentum, there was a lot of doubt during the month regarding the prospects for the AI sector in the near term. One protagonist here was Dr. Michael Burry, who is known for successfully betting against the US housing market in the Global Financial Crisis and whose character featured in the Hollywood movie “The Big Short.” During the month, it came to light that Burry had taken out a large amount of put options on Nvidia and Palantir. Investors buy put options on a stock when they expect the stock to fall. One issue that Burry, and many other investors have, is that investor exuberance around AI has driven valuations to high levels. Another issue is hyperscaler depreciation. Some investors are concerned that hyperscalers are increasing the "useful life" they assign to AI hardware (e.g., Nvidia's GPUs) for depreciation purposes, stretching it from around three years to five or six years (and artificially inflating their short-term profits). If these hardware products become obsolete faster, it could force these companies to make massive write-downs. This could lead to a sharp contraction in AI spending and negatively impact suppliers such as Nvidia and AMD.

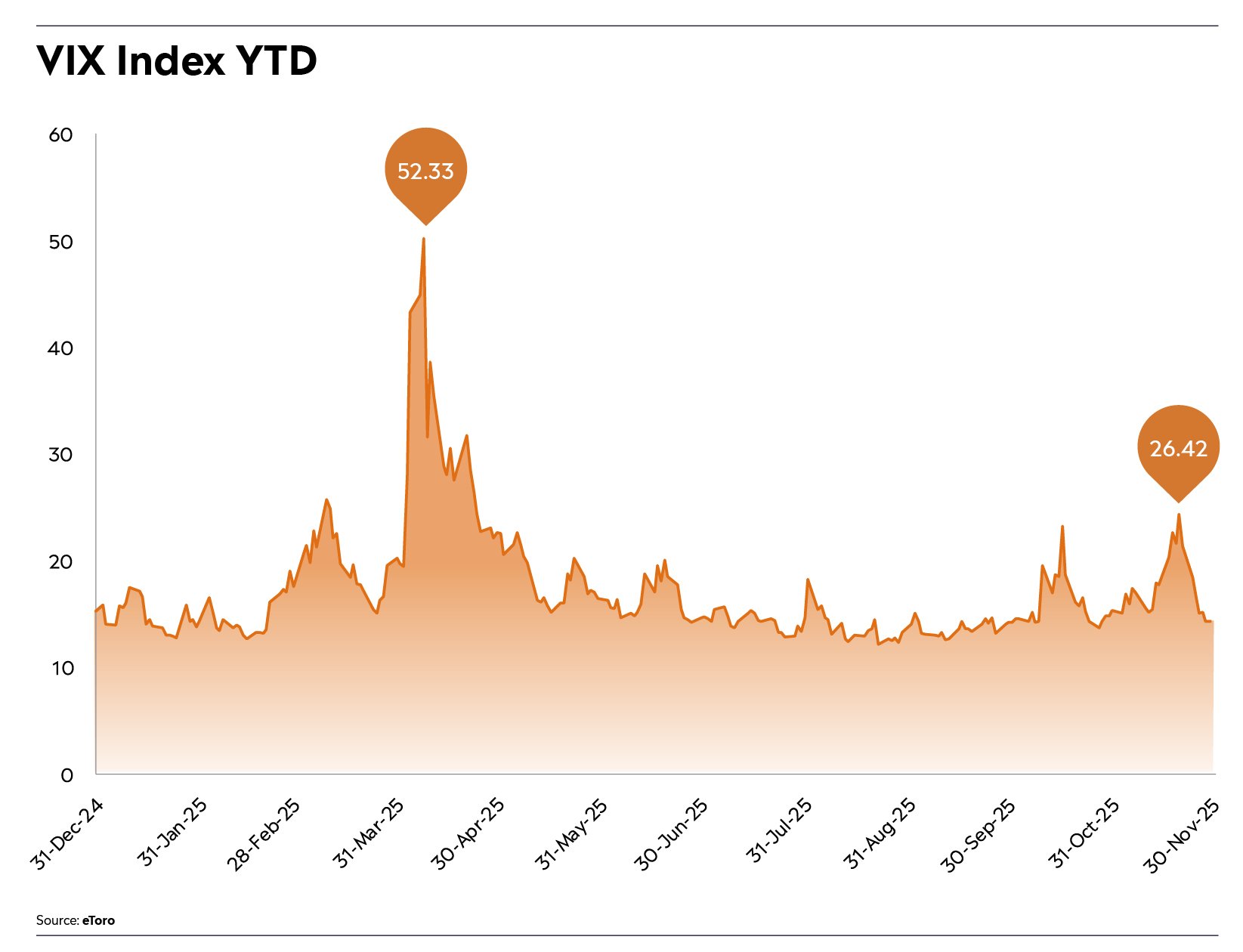

It’s worth noting that after Nvidia’s earnings, the market experienced a sharp pullback, despite the fact that the company beat estimates and raised its guidance. The concerns around a potential AI bubble were certainly a driver here. However, there were also a few other factors at play. One was the belief that the US Federal Reserve won’t cut rates in December. Another was a meltdown in the crypto market, which may have forced leveraged crypto traders to sell stocks to cover margin calls. During this pullback, the CBOE Volatility Index (VIX), which measures investor fear levels, rose to 26.42. This was the highest level since the market sell-off in April, when it spiked to 52.33.

Zooming in on the Magnificent 7

Alphabet was the star performer in November, rising 13% and overtaking Microsoft in market cap. It shot up after it came to light that Warren Buffett’s investment firm, Berkshire Hathaway, invested in the company in Q3. It then moved higher after the release of Gemini 3.0 and Nano Banana Pro, which are both extremely powerful AI products and on par with those from OpenAI. One other factor that boosted Alphabet stock was rumours that Meta is planning to use its TPU chips for AI (which sent Nvidia stock down to three-month lows).

In the Chinese tech space

Baidu made headlines after it held its Baidu World 2025 conference. Here, the company released ERNIE 5.0, the latest version of its AI model. ERNIE 5.0 can jointly model text, images, audio, and videos and has 2.4 trillion parameters, meaning that it is one of the largest and most multimodal foundation models in the world. Another highlight of the conference was the release of two new AI chips – the Kunlun M100 and M300. Zooming in on Baidu’s robotaxi segment, Apollo, this is now processing 250,000 orders a week and to date, has provided 17 million rides globally (more than any other robotaxi company in the world).

Away from tech, the Healthcare sector had a really strong month.

It has underperformed this year due to policy headwinds and drug pricing scrutiny. However, it now appears to be playing catch-up. One reason investors are suddenly becoming more interested in this sector is that historically healthcare has been quite defensive (e.g., people are always going to need vaccines). At the same time, however, there is plenty of innovation in this space. From GLP-1 weight-loss drugs to robotic surgery technology, there are a lot of long-term growth drivers.

On the economic front

US interest rate cuts were in focus in November with traders closely scrutinising comments from Federal Reserve officials for any signals regarding the timing and magnitude of future easing. At one stage, the odds of a December rate cut fell to 40%. However, in a major reversal, the odds of a cut before the end of 2025 rose to around 80% by the end of the month. The jump in expectations came after New York Fed President John Williams said further policy easing may be appropriate.

In the commodities space

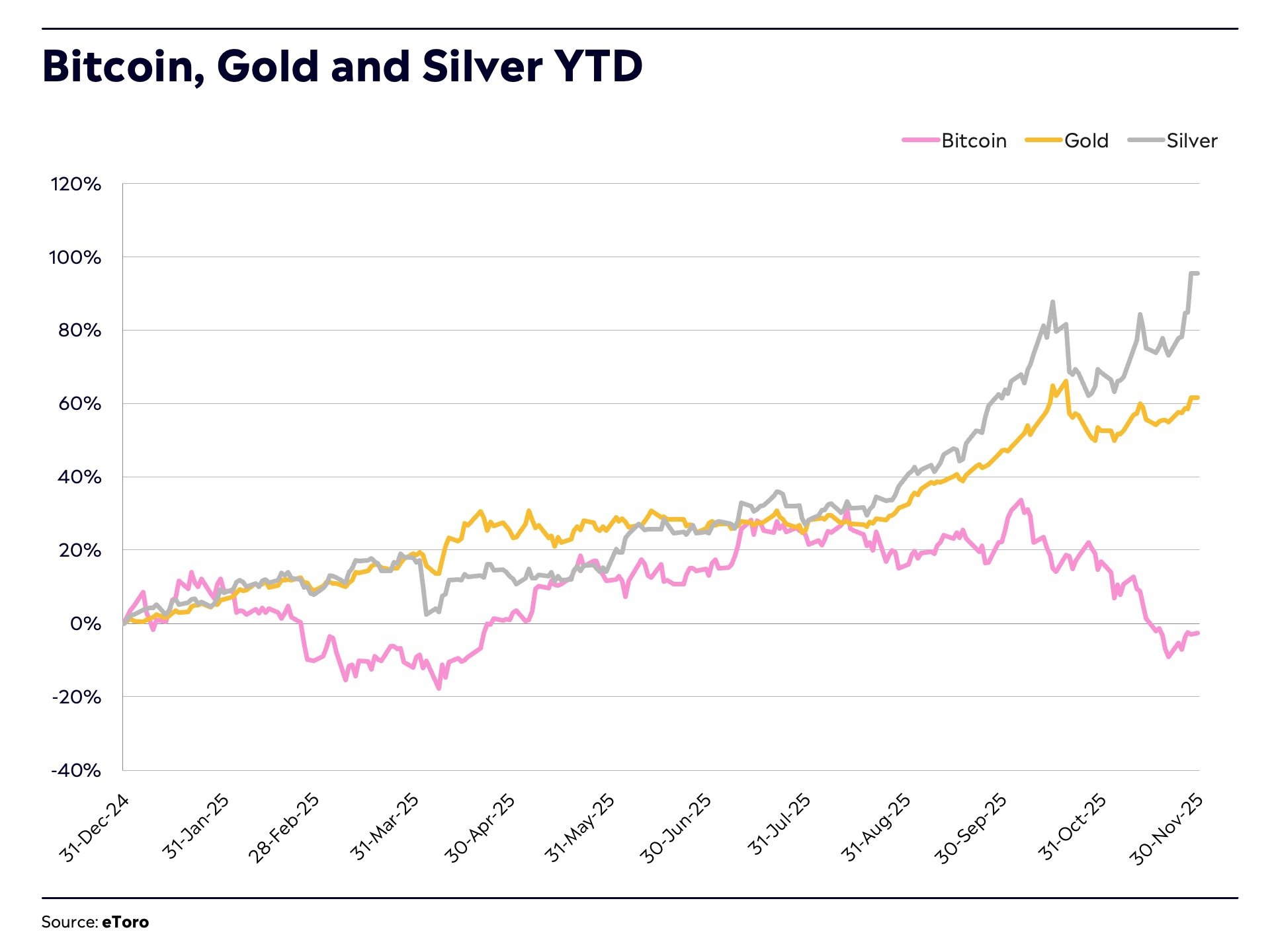

Oil fell below $60 per barrel, ending the month near $59 per barrel. While this put pressure on oil stocks, it should help to ease inflation, and potentially support interest rates cuts. Gold had a good month, rising about 5%. It ended the period near $4,200 per ounce. Silver – which has more than doubled in price this year – outperformed gold again. It rose almost 20%, ending the month above $56 per ounce, at its all-time high level.

Finally, turning to crypto

It underperformed in November with Bitcoin falling around 17% to $91,000 and Ethereum declining approximately 22% to $3,000. At one point, Bitcoin was trading at $82,000 – not far off from its previous level when Donald Trump won the US election in 2024 – while Ethereum was under $2,700. The weakness here was caused by a range of factors including liquidations by whales, large ETF outflows, concerns that stablecoins were now doing a lot of the things Bitcoin was meant to do, and general risk-off sentiment. It’s worth pointing out that while crypto prices have fallen, the earnings of many companies in the crypto ecosystem have been strong. For example, Coinbase and Galaxy Digital all recently reported record revenues for Q3.