Covering September Market

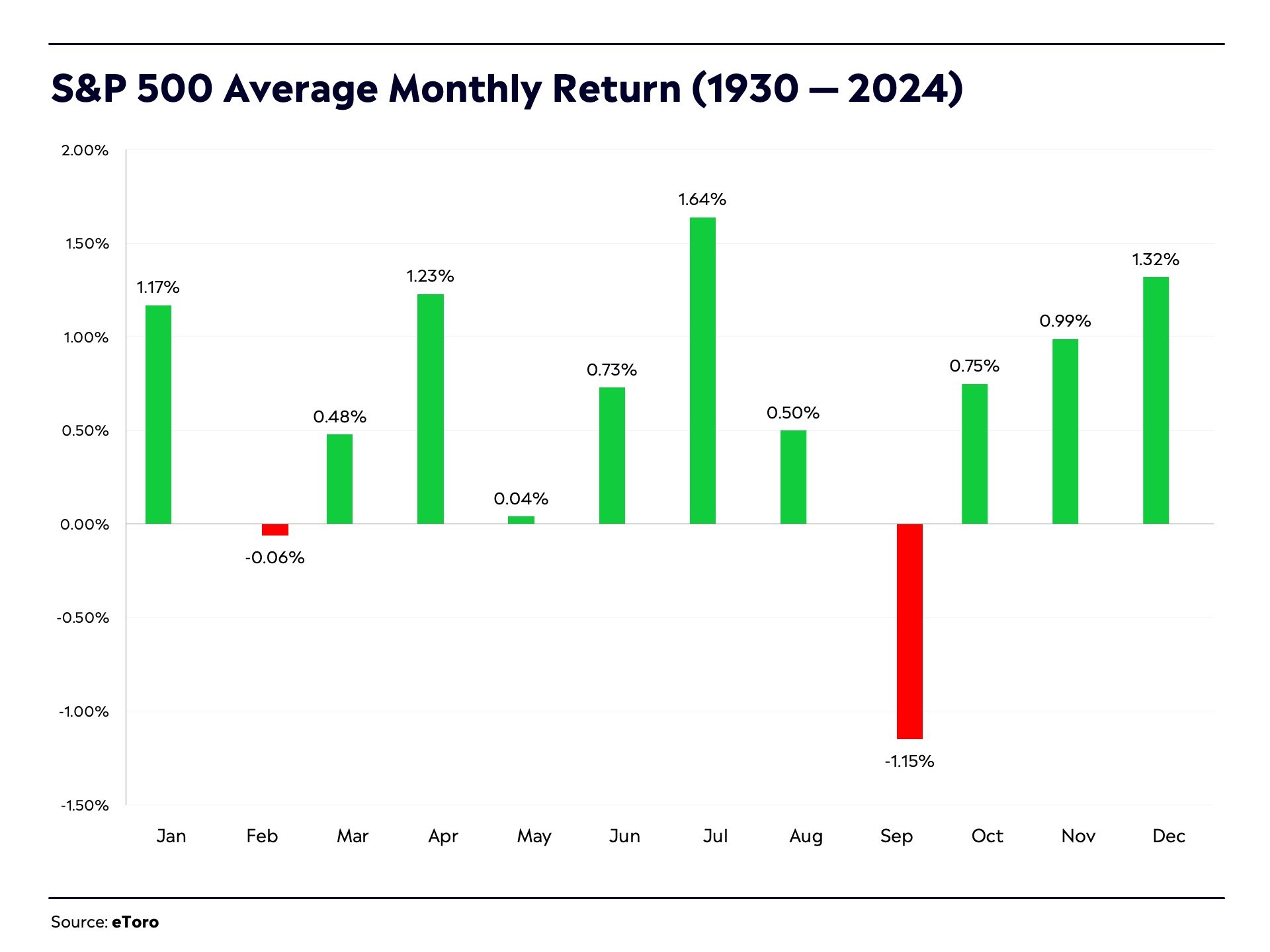

September is often a weak month for stocks, but this year, markets bucked the trend.

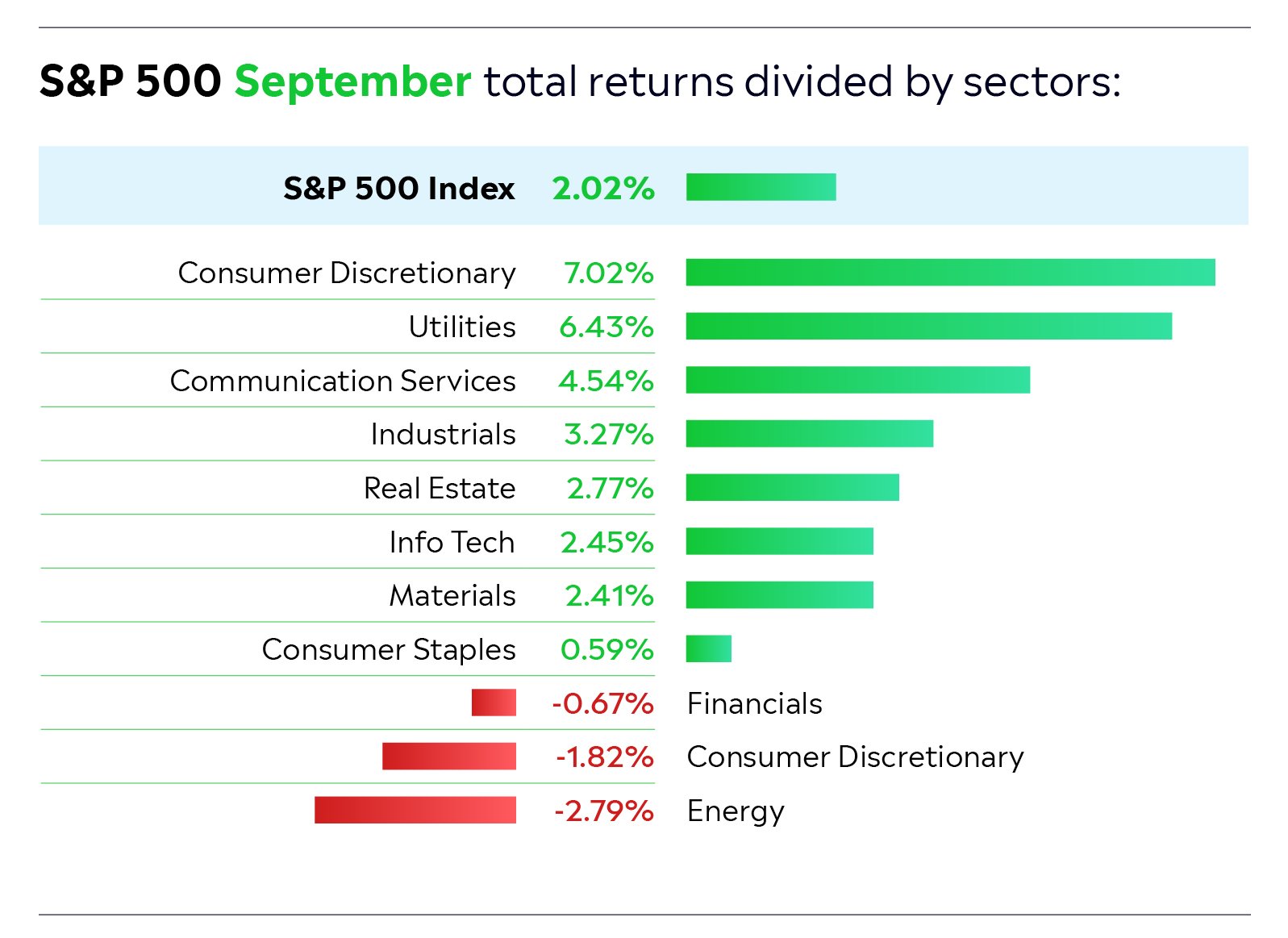

Helped by a 50 basis point interest rate cut by the US Federal Reserve, major indexes such as the S&P 500 and the Dow Jones Industrial Average overcame volatility early in the month to hit new all-time highs. The best-performing sectors were Consumer Discretionary and Utilities, which should benefit from lower interest rates. Energy — which took a hit due to falling oil prices — and Healthcare were the biggest underperformers.

The month got off to a rough start when US stocks experienced a sharp pullback on the first trading day of September. This pullback was mainly the result of weak Purchasing Managers Index (PMI) data, which led to concerns that the US could be heading towards a recession.

One of the worst hit stocks was chip designer Nvidia, which fell 9.5% and lost around $280 billion in market cap.

This was a record one-day wipeout for an American company. Nvidia’s share price recovered later in the month, however, after CEO Jensen Huang talked up demand for the company’s artificial intelligence (AI) chips at a Goldman Sachs conference. Huang said that demand for Nvidia’s next-generation Blackwell chips is high and that major tech companies are desperate to get their hands on them.

It was a turbulent month for AI and chip stocks in general with rapid shifts in sentiment at times.

Broadcom, for example, saw its share price fall 10% in a day after its revenue forecast for the current quarter spooked investors. It ended the month in the green, however, as sentiment towards AI businesses improved. Shares in Micron, which specialises in memory and storage solutions, jumped late in the month after the company said that high bandwidth memory was sold out for calendar year 2024 and 2025. Super Micro Computer stock ended the period down after a Wall Street Journal report claimed that the company — which was hit by a short seller report in August — is being probed by the US Department of Justice (DoJ).

As for Intel — which has been left behind by Nvidia in the AI chip race recently — it had an eventful month.

After a dip early in September, the stock jumped when the chipmaker announced plans to turn its manufacturing foundry business into an independent unit and advised in a separate announcement that it had entered into a deal with cloud computing giant Amazon to produce custom AI chips. It then jumped again on the back of talk that Qualcomm is reportedly interested in a friendly takeover and that private equity firm Apollo Global Management is willing to make a $5 billion equity investment in the company. If a deal did go though, it would be one of the biggest tech deals ever.

Zooming in on Big Tech stocks, it was a mixed month here.

Meta Platforms was up strongly (and hit new all-time highs) on the back of excitement around its smart glasses. Tesla also rallied hard ahead of its October 10 robotaxi event. The value of Microsoft rose after the company announced a 10% increase in its quarterly dividends and approved a new $60 billion stock buyback program. Apple ended the term slightly positive despite the fact that the new AI-ready iPhone 16 hit stores later than expected all around the world (analysts have been debating whether delays in the AI features have hurt demand for the new device). Alphabet experienced a significant decline early in the month on the back of concerns over regulatory intervention before making a sharp, V-shaped recovery in the second half of September.

US Federal Reserve cutting interest rates

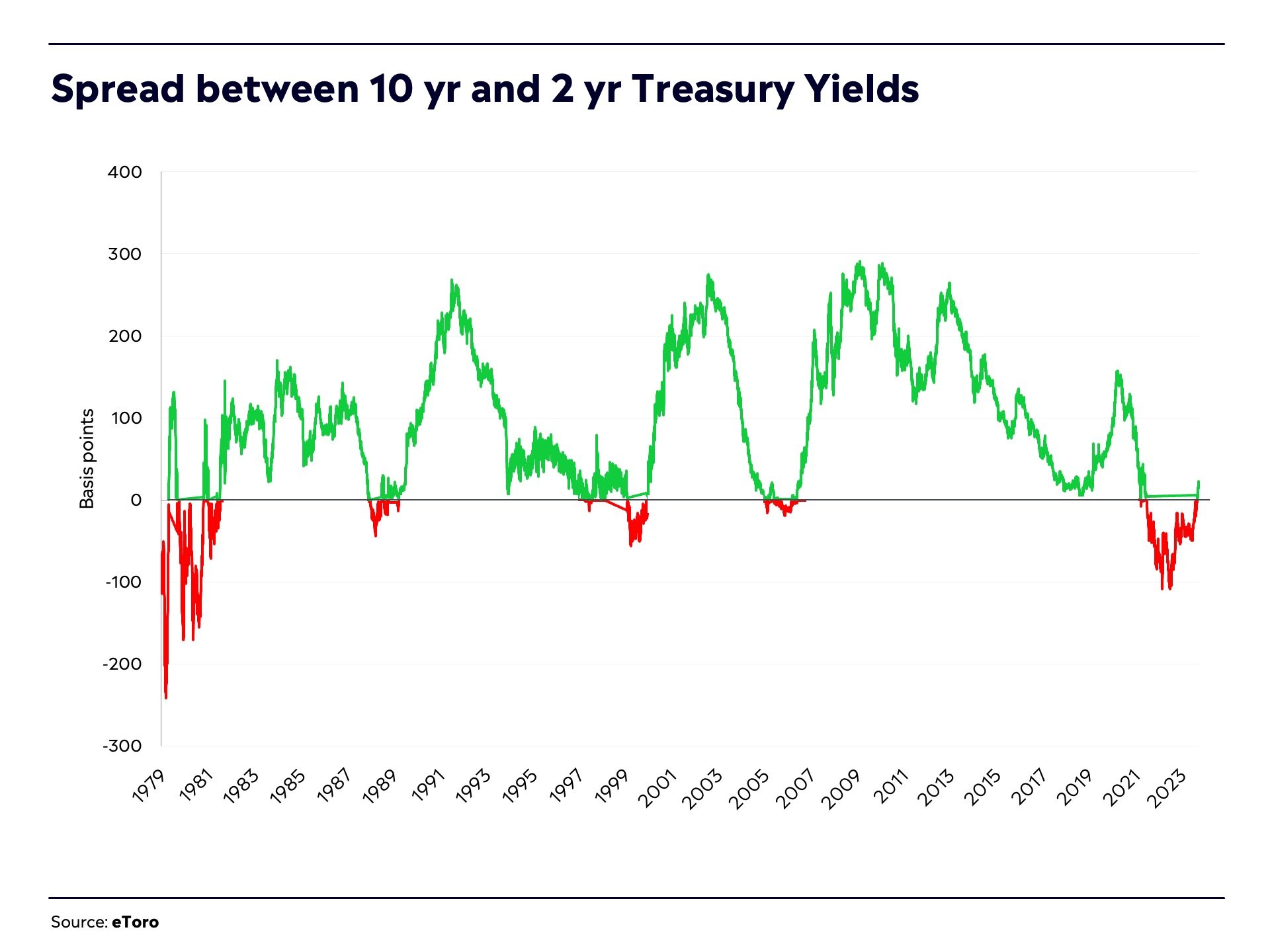

In the first couple of weeks of September, there was much focus on whether the US Federal Reserve would cut interest rates by 25 or 50 basis points at its September 17–18 meeting. The Fed ended up cutting by 50 basis points (to a range of 4.75%–5.00%), with the central bank stating that a larger cut was needed amid cooling inflation and increasing job market concerns. The outsized rate cut by the Fed — its first cut in more than four years — increases the chance of a “soft landing” in the US, and stocks subsequently had a strong positive reaction to the cut. Investors were happy to see the spread between 10-year and 2-year Treasury yields come back into positive territory, as longer horizon yields are normally higher than shorter-term yields, except when there are recession fears. US GDP for Q2 came in at 3% — above expectations. GDP is considered backward looking, however, projections show the economy has been growing at a steady pace in Q3.

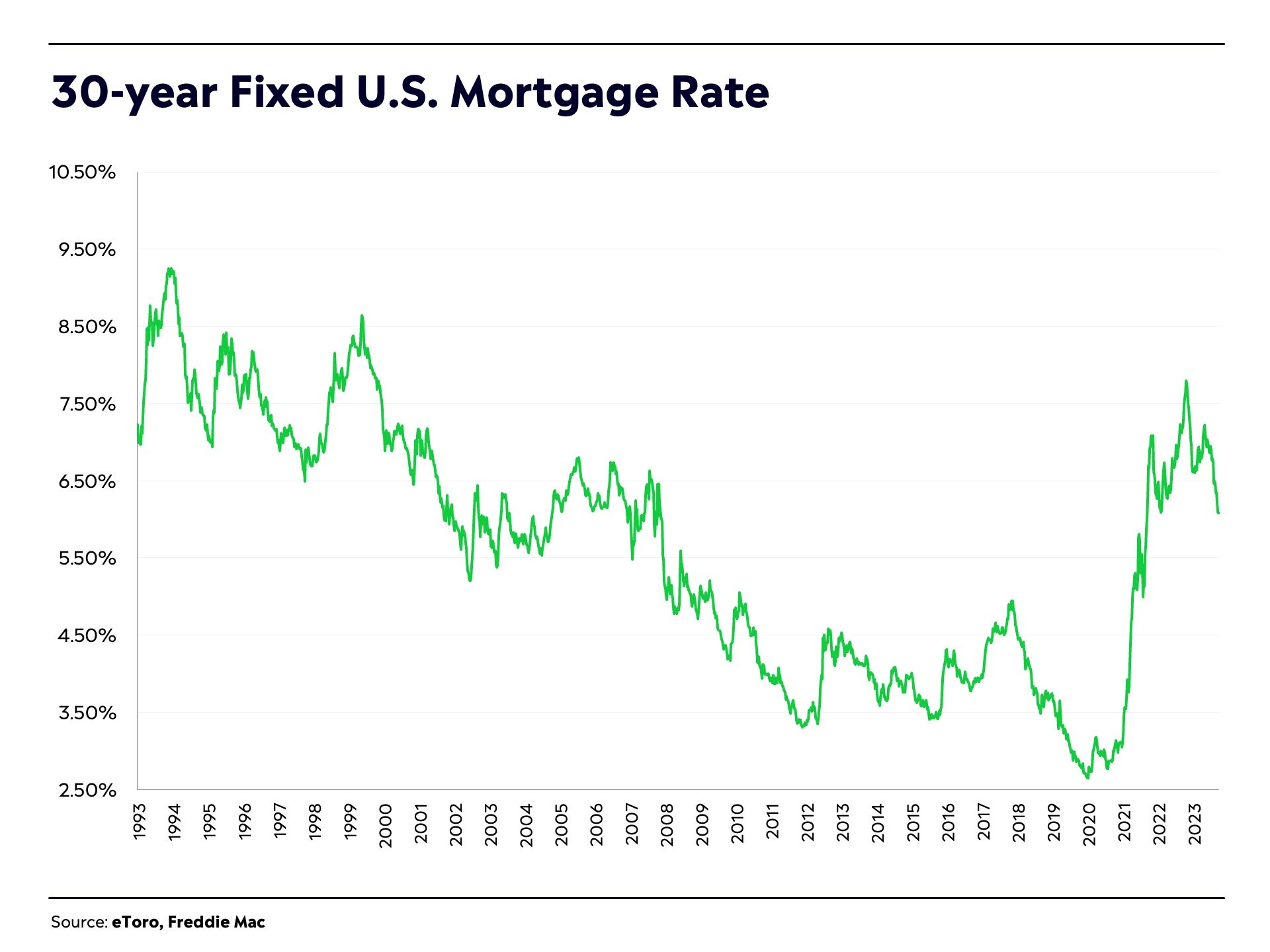

Looking ahead, economists expect US interest rates to fall by more than two full percentage points from their recent highs over the next 12 months (to between 3.25% and 3.50% by mid-2025), which would be the steepest drop outside of an economic downturn since the 1980s. As a result of the Fed’s move, the 30-year mortgage rate in the US moved down to 6.0% — the lowest rate since February 2023.

Lower-interest rate environments help the real estate industry, as well as other capital intensive sectors such as renewable energy and Utilities.

It’s worth noting that in the political space, Kamala Harris and Donald Trump had their first debate during the month.

After the event, the general consensus was that Harris put in a stronger performance than Trump as she frequently rattled the former president. However, polls and betting markets are currently very tight. You can read more about the potential impact of the US election results in the trends section of this report.

Away from the US, the Chinese economy continued to deteriorate, with forecasts lower than expected for industrial production and retail sales. In China, the real estate industry is still in turmoil and house prices are falling. Late in the month, however, Chinese stocks surged as the People's Bank of China (PBOC) unveiled an aggressive package of stimulus measures designed to revive the Chinese economy. The measures included a substantial cut to bank reserve requirements, as well as a 50 basis point cut to existing mortgage rates. During the month, China’s electric vehicle sector made headlines after the Biden administration proposed banning Chinese software and hardware in connected vehicles on American roads due to national security concerns. The planned regulation would force American and other major automakers to remove key Chinese software and hardware from vehicles in the US in the years ahead.

Elsewhere in Asia, the Japanese yen appreciated in September (a trend that started in July when it peaked at 161 to the US dollar). It momentarily crossed below the 140 yen per dollar mark before ending the month near 144 to the greenback. Economists expect the Bank of Japan (BoJ) to continue increasing rates, but most likely not until 2025. That’s because Governor Kazuo Ueda has signalled that the BoJ needs to be confident that the US economy will experience a soft landing.

In Europe, Italy’s UniCredit announced that it’s trying to build a big stake in, and possibly acquire, Germany’s Commerzbank. Currently, it has a 21% stake, and it has submitted a request to increase that to 29.9%. Bank analysts believe that a deal could lead to a higher level of profitability for the two European banks. However, the German government — which was caught off guard by the news and firmly opposes a deal — may block a takeover.

Turning to commodities, gold hit a new all-time high of $2,670 as a result of the aggressive 50 basis point rate cut by the Fed and expectations of further rate cuts (lower yields make gold more attractive as an investment). The precious metal closed the month around $2,630, up approximately 27% for the year.

Oil, on the other hand, had a weak month, falling to $68 dollar per barrel at one stage — the lowest level of the year. It briefly rebounded on hopes of a stronger Chinese economy and as a result of geopolitical instability in the Middle East, but then fell again after Saudi Arabia said that it would return to higher oil output and abandoned its $100 per barrel crude target.

As for crypto, it was a good — yet volatile — month.Early in September, Bitcoin and Ethereum experienced significant weakness amid the high level of volatility in the stock market with Bitcoin ETFs experiencing their largest single-day outflows in four months. However, Bitcoin recovered in the second half of the month to finish up at about 8%.

Looking ahead, the outcome of the US election could have implications for Bitcoin and other cryptoassets. Recently, Donald Trump has been courting the votes of crypto enthusiasts by promising to make America “the crypto capital of the planet” and saying that he will create a strategic national Bitcoin stockpile similar to the US government’s gold reserves.