Covering October Market

October was a choppy month for stocks with most major indexes ending the period down slightly.

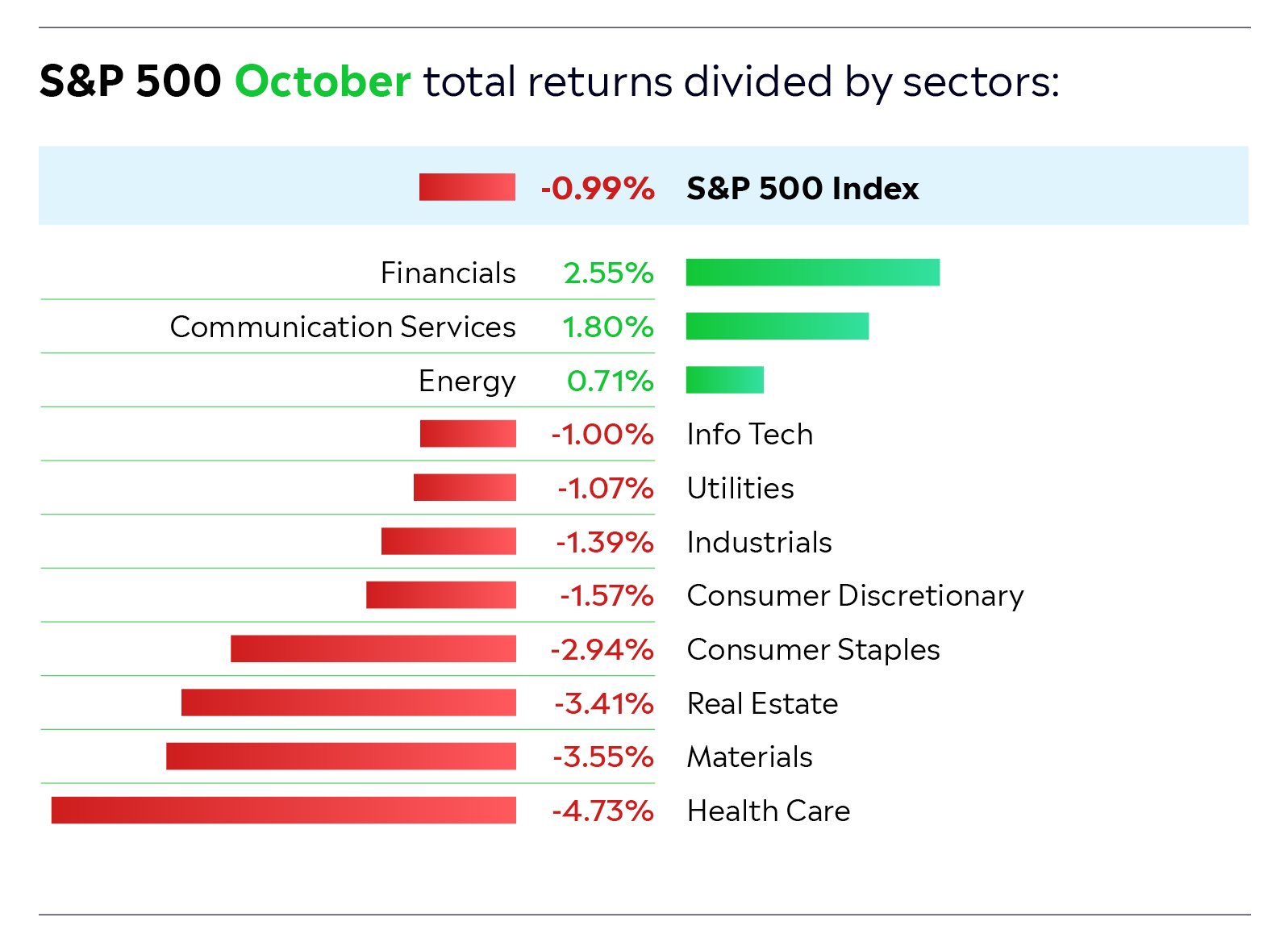

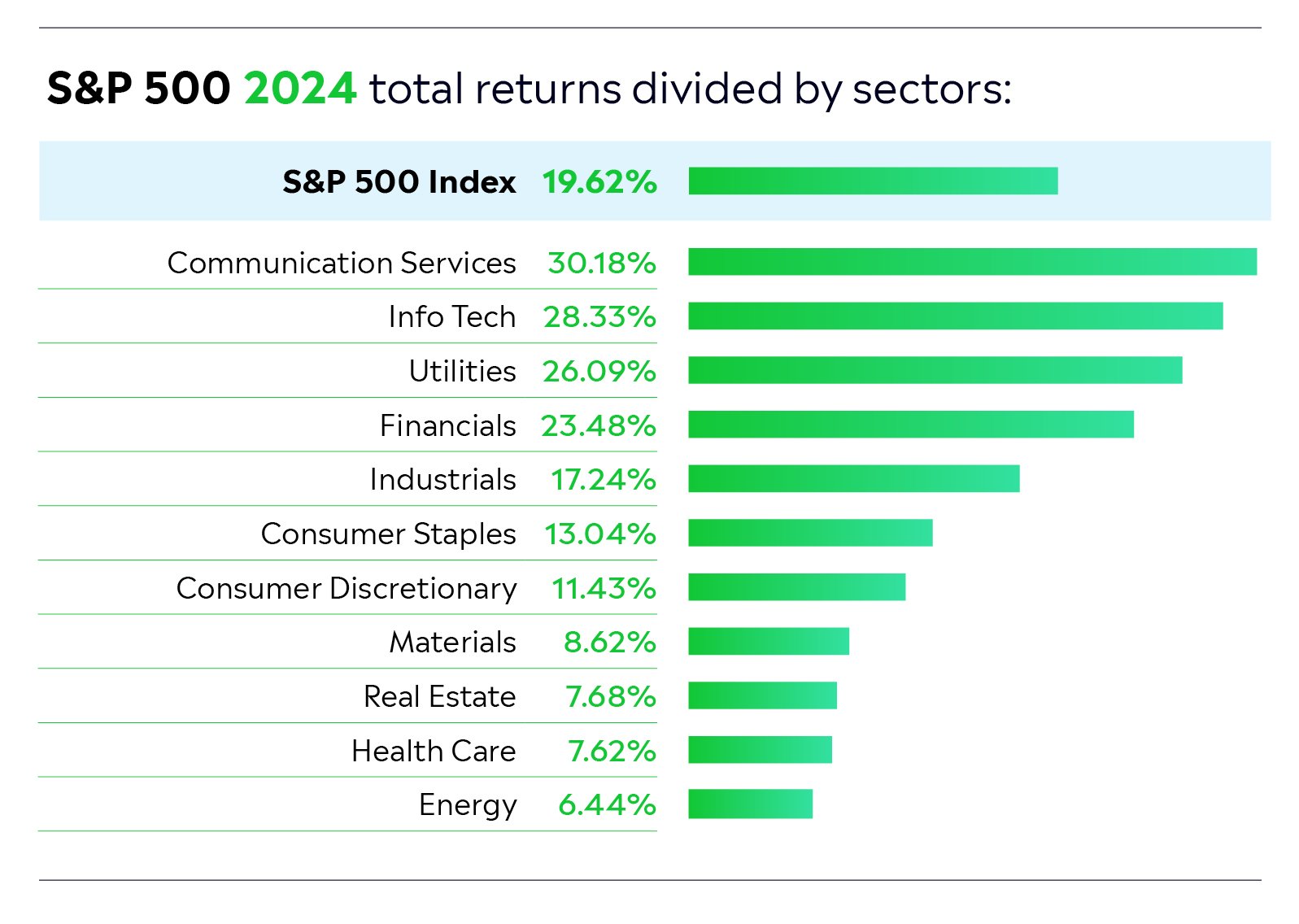

Throughout the month, investors had a lot to digest, including geopolitical conflict, US election uncertainty, commodity price volatility, and Q3 corporate earnings. The best-performing sectors for the period were Communication Services, and Financials. Healthcare lagged at the other end of the spectrum.

The month got off to a rocky start due to the conflict in the Middle East. With missile attacks in focus, share prices were volatile. Equity markets showed strength in the second half of the month, with the S&P 500 and the Dow Jones Industrial Average— both of which have been in “bull markets” for over two years now — hitting new all-time highs despite ongoing geopolitical and election uncertainty. However, late in the month, investor sentiment deteriorated and stocks pulled back.

In relation to the election, there was little clarity for investors in October as polls showed no clear winner. Much focus was on the so-called “swing states” such as Pennsylvania and Michigan, which can have a major impact on the result.

In recent days, it has been announced that Donald Trump will be the next US president.

A Trump administration is likely to benefit Big Tech, oil and gas, and defence stocks, but could result in more tension between the US and China.

Zooming in on individual stocks, Tesla was in focus in October, as it held its long-awaited robotaxi event on the 10th. Going into the event, investors were expecting the company to reveal multiple robotaxi prototypes, an app for consumers, and details in relation to launch dates and potential revenue. However, while Tesla did reveal two different robotaxi prototypes (a 2-seater car and a 20-person van) at the event, there was no app, and details in relation to the launch were vague. As a result, investors dumped the stock, leading to a sharp decline in the share price (and a big gain for rival Uber). Tesla’s share price rebounded spectacularly later in the month, however, after CEO Elon Musk told investors during the Q3 earnings call that he is expecting 20–30% revenue growth next year. This led to a 22% jump in the share price — the best day for the stock in over a decade — and added close to $150 billion in market cap.

Another stock that shot up after Q3 results was Netflix. It beat earnings estimates comfortably and grew subscribers significantly over the quarter. One factor that has been helping this company recently is digital advertising as it now offers an ad-tier option for users. During the month, the stock hit new all-time highs above $750, which is impressive given that in mid-2022 it was trading near $175.

Elsewhere in the large-cap tech space, Alphabet produced a strong set of Q3 results that were well ahead of estimates. It benefitted from strong growth in its cloud computing division, which saw year-on-year growth of 35% thanks to new artificial intelligence features.

As for semiconductor companies, results were mixed. Taiwan Semiconductor Manufacturing Company Limited (TSMC) — which manufactures chips for a range of companies — posted strong quarterly results and signalled continuous robust demand for its AI chips. This sent the stock up nearly 10% (and boosted other chip names). However, Dutch company ASML, which makes complex equipment for chip manufacturers that allows them to print microscopic designs on silicon wafers, posted poor results after a few customers delayed orders. This led to a sharp pullback in the share price and allowed Germany’s SAP to overtake the company in market cap and become the largest European tech company. During the month, Nvidia hit new all-time highs and briefly became the world’s most valuable company again before Apple got the throne back. However, rival AMD lost ground after investors were unimpressed with its Q4 guidance.

In banking, earnings were generally good. Goldman Sachs delivered beats on revenue and earnings as a pick up in stock trading and investment banking boosted its performance. Meanwhile, JP Morgan also beat expectations thanks to a strong performance in investment banking. Both stocks hit new all-time highs during the month.

Looking beyond earnings, one notable event during the month was Hurricane Milton in the US. This boosted stocks such as those of United Rentals and Ashtead Group, which rent out power generators and other construction equipment, while negatively impacting insurers with significant exposure to Florida. Another key event was the fifth Starship launch by Elon Musk’s space company SpaceX. The rocket made history after its “super heavy” booster returned to land in the arms of the company’s launch tower just minutes after launch.

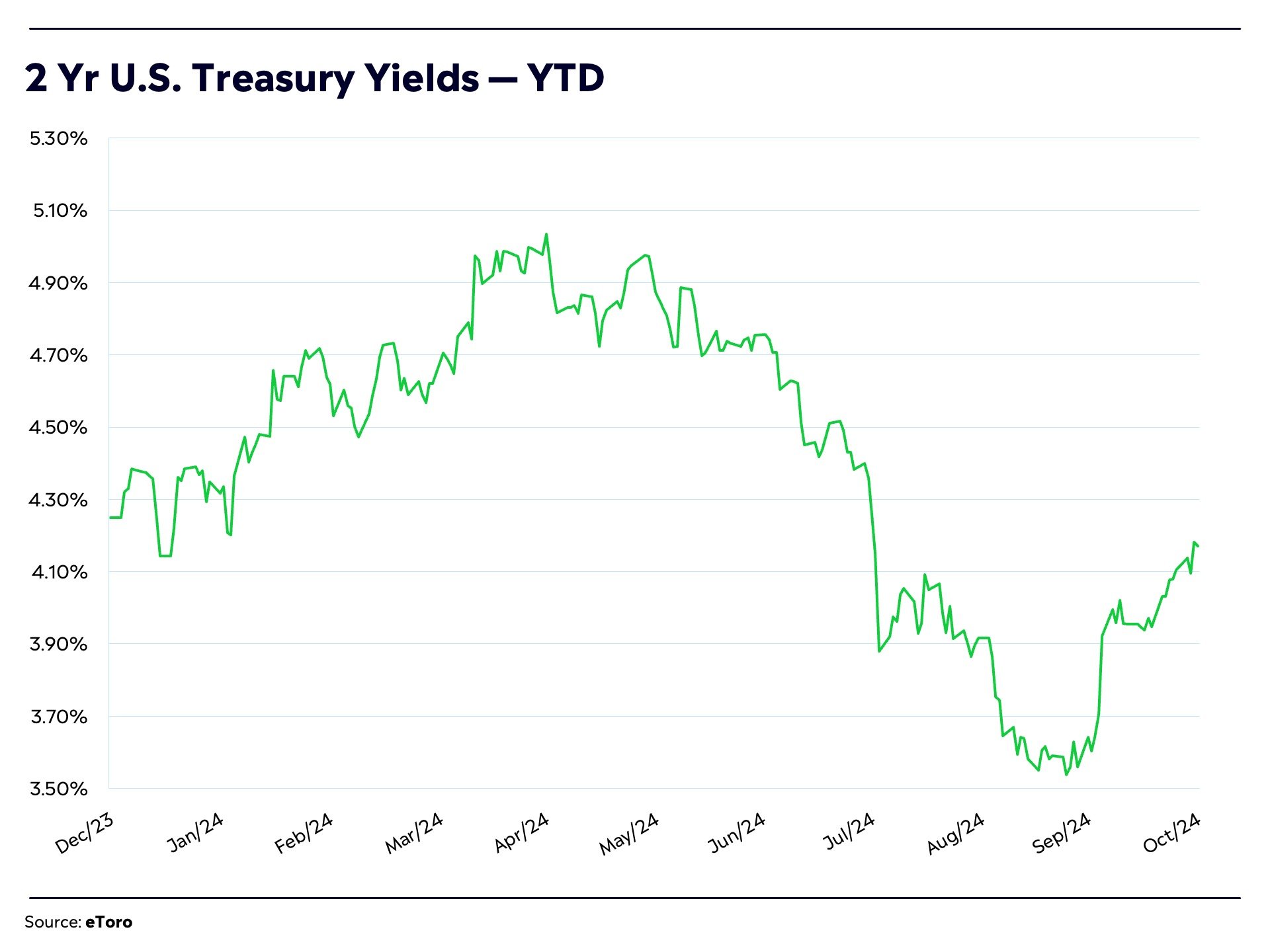

Moving on to economic data, the US added 254,000 jobs in September — well ahead of the Dow Jones consensus forecast of 150,000. Meanwhile, the unemployment rate dropped to 4.1%, a level last seen in June. This data — and concerns about future government policies increasing inflation — sent US 10-year Treasury yields up from 3.78% to around 4.28%. Two-year yields climbed to 4.17%, a level approximately 45 basis points higher than the rate after the September rate cut.

In Europe, the European Central Bank (ECB) cut interest rates for the third time this year, taking the deposit rate down by 25 basis points to 3.25% and sending the GBP/EUR exchange rate momentarily up to its highest level in more than two years. The central bank’s communication was more dovish than anticipated, and markets are now pricing in a chance of a 50-basis-point cut in December.

The Bank of Canada also cut rates, announcing a 50-basis-point reduction due to the fact that inflation is now lower than the central bank’s 2% target. The Bank of Japan kept rates steady, but flagged global risks.

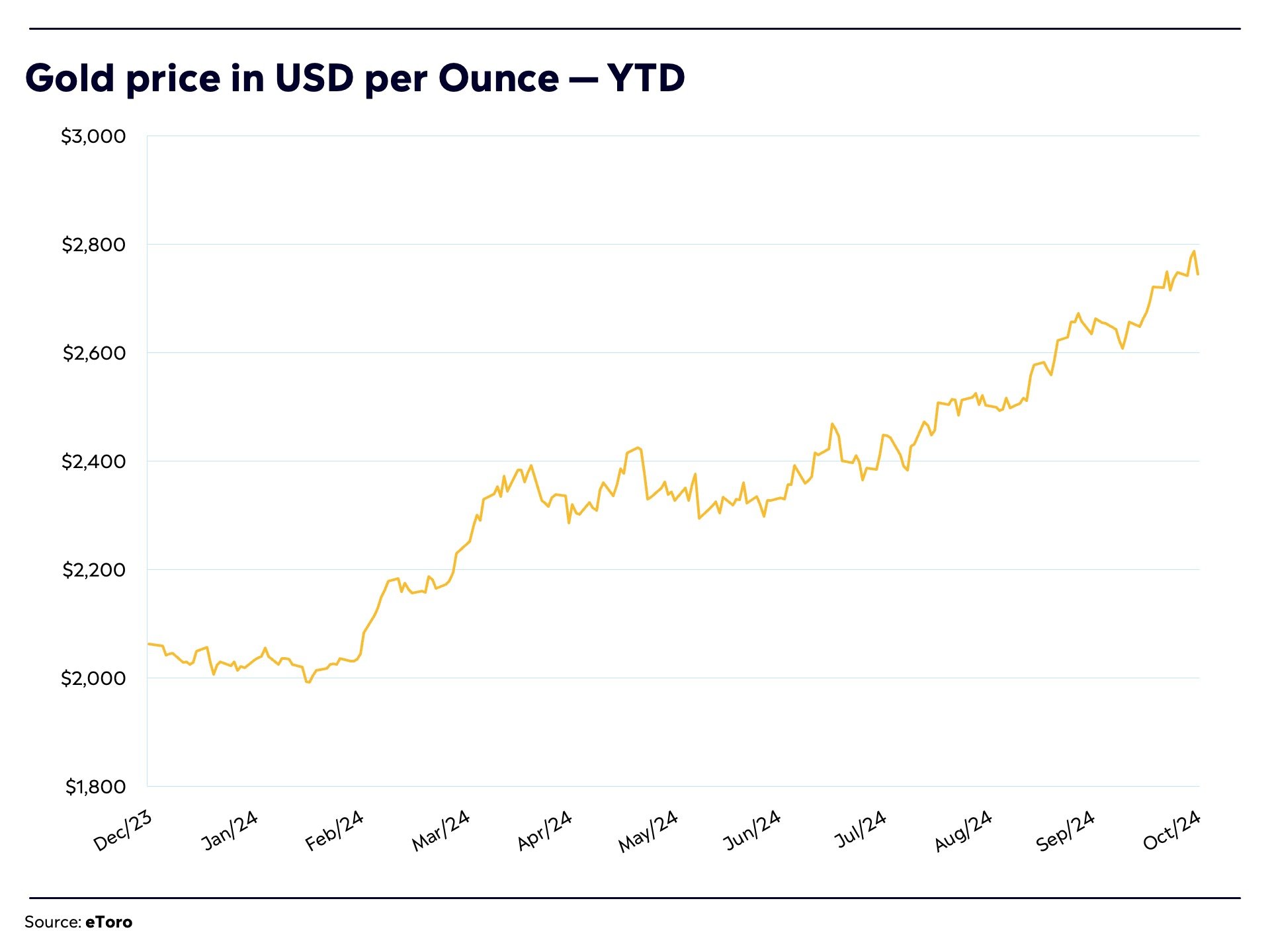

In the commodities space, during the month, gold hit new all-time highs of $2,790, closing positive for the 9th consecutive month. As a safe-haven asset, it benefitted from the tight US election race and geopolitical uncertainty.

As for oil, it was a volatile month with WTI prices shooting up 8% to $77 per barrel in the space of five days early in the month as traders worried about escalating Middle East tensions — before plummeting later in the month after Israeli airstrikes avoided Iran's oil facilities. WTI ended the month at $69 — well below its 2024 highs.

Finally, it was an excellent month for cryptoassets.

Bitcoin prices surged, rising close to $73,000 at one point — thanks to a spurt of inflows into Bitcoin exchange-traded funds (ETFs) as well as belief that a potential Trump administration could support crypto prices.

Trump is pro-crypto, so much so that Bitcoin is now viewed as a “Trump Trade."

Ethereum also gained, but not as much as Bitcoin.