Covering November Market

November was a strong month for global equities, however, not all regions produced gains for investors.

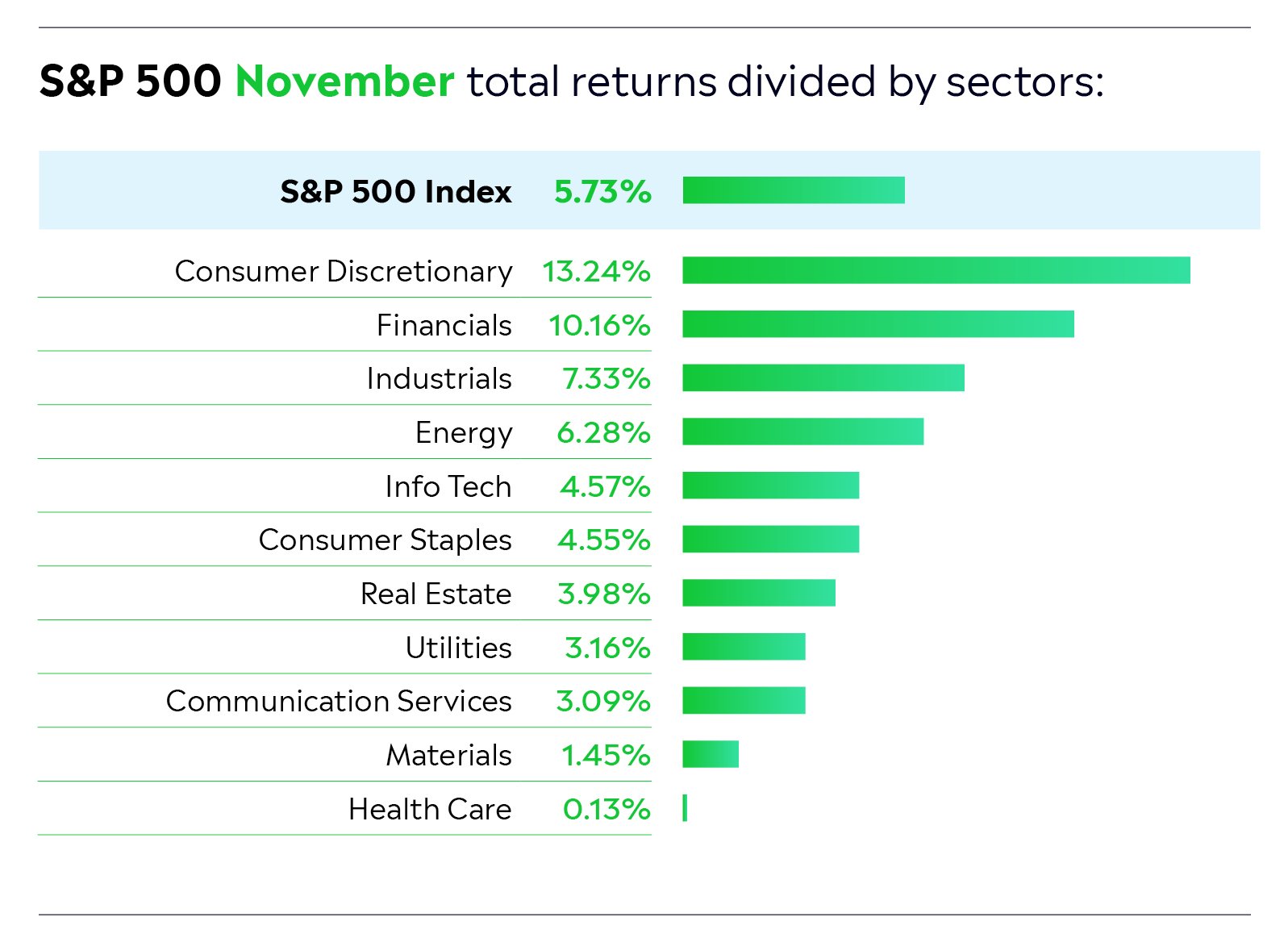

While US stocks surged on the back of Donald Trump’s win in the US election, European, Japanese, and Chinese shares lost ground. The best-performing sectors of the period were Consumer Discretionary and Financials, with over double-digit performance each. At the other end of the spectrum, Healthcare was flat.

Donald Trump’s decisive victory in the US election was a pivotal moment for the market in November.

In the lead-up to the event, there was a degree of uncertainty due to the fact that polls were tight. As a result, many investors were in a cautious mood. However, investor sentiment swiftly improved after his victory. Given that Trump is stock market and economy-friendly, investors piled into equities in the days following the election result. This led to a so-called “everything rally,” with significant gains in many areas of the market. The Dow Jones Industrial Average and the S&P 500 Index closed November at their all-time highs.

Financial and technology stocks soared amid expectations of less regulation and more M&A activity under a Trump administration.

This backdrop should support a range of businesses within the financial sector, including banks, private equity firms, and crypto businesses. It should also be beneficial for Big Tech companies, which have been subject to antitrust regulation in recent years, as well as small- and mid-cap technology companies, many of which could now be M&A targets. Another area of the market that did well was travel. Investors are now anticipating a strong US economy in the years ahead and this has boosted stocks such as Marriott, Booking Holdings, and Disney. Oil and gas and defence also outperformed as Trump has historically favoured these industries.

However, some areas of the market struggled after Trump’s win. Renewable Energy — which is likely to get less support under a Trump administration — was one such area. Pharmaceuticals also underperformed after it came to light that vaccine skeptic Robert F. Kennedy Jr. had been appointed as the head of the US Department of Health and Human Services. Several other sectors and markets underperformed amid concerns about new tariffs. Trump has said that he will impose additional 10% tariffs on goods from China and 25% tariffs on all products from Mexico and Canada. These tariffs could hit the bottom lines of US automakers, especially General Motors (which manufactures vehicles in Canada and Mexico), and raise prices of SUVs and pickup trucks for US consumers.

It’s worth noting that in the week after the election, bond yields rose sharply, eradicating some of the gains from the Trump rally.

Concerns over higher inflation under a Trump Administration were the key driver of the increase in yields — and many economists now expect the pace of interest rate cuts will be slower than previously expected. Some analysts, such as BofA’s Michael Hartnett, believe that it’s time to move capital from US stocks to European and Chinese stocks. Hartnett believes that China will ease fiscal policy and Europe will cut rates aggressively in anticipation of Donald Trump’s upcoming tariffs.

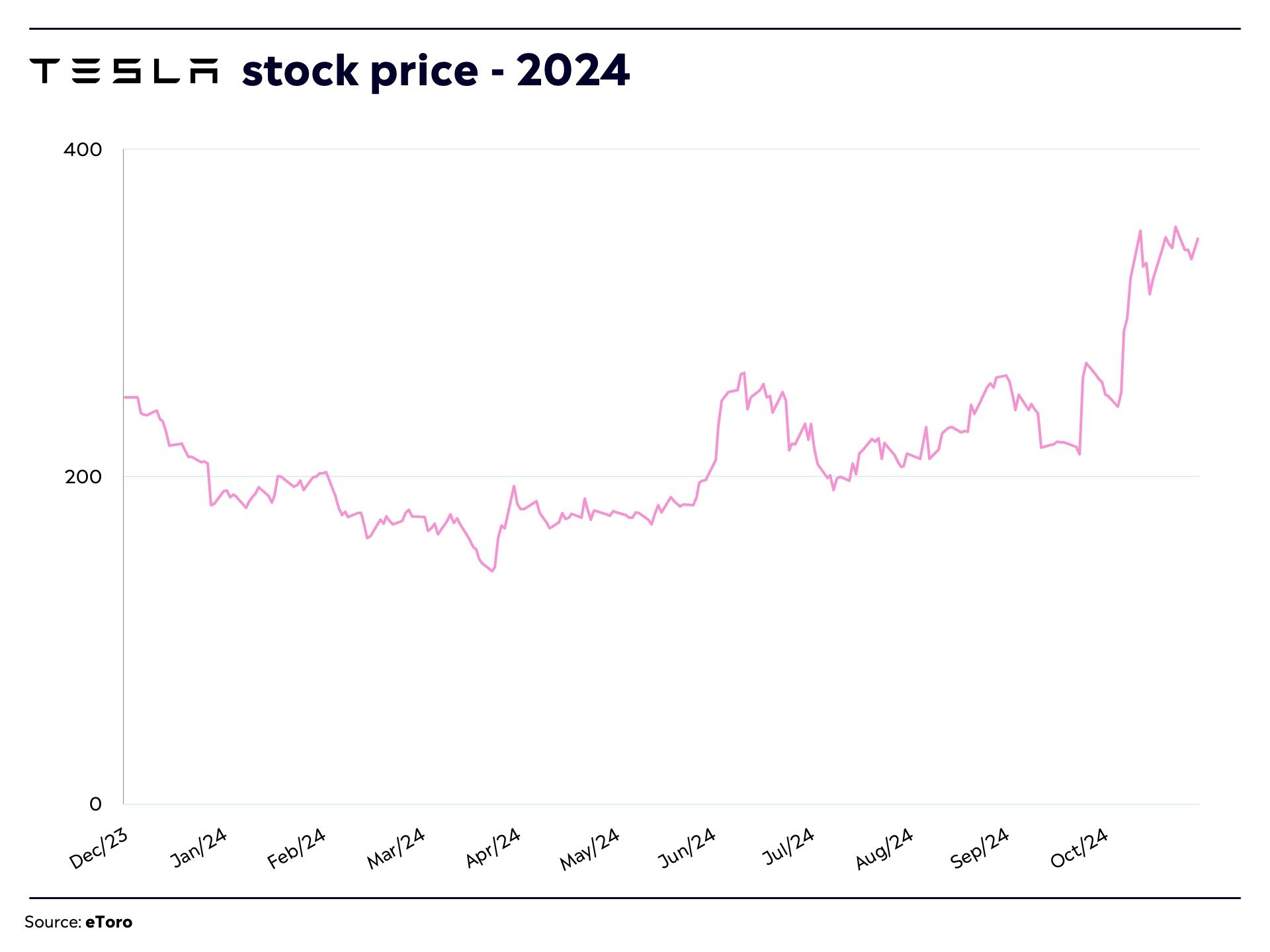

Within the “Magnificent 7,” there were some notable developments during the month. Tesla stock shot up after the election due to the fact that Tesla CEO Elon Musk is going to be working with Trump to boost government efficiency. Many investors believe that with Trump in power, Tesla could have its self-driving cars on the road sooner than previously expected. Nvidia posted its Q3 results, and the figures were once again exceptional, with year-on-year revenue growth of 94%. However, the stock — which had rallied more than 40% in the lead-up to the print — saw some profit-taking after earnings. Alphabet stock fell after the US Department of Justice (DoJ) ordered the company to sell Chrome, the world's most popular web browser. According to the DoJ, Google operates an online search monopoly.

Software was where a lot of the action was for tech investors though.

In the first three quarters of 2024, software was held back by a range of factors, including uncertainty over the election and the economy. The sector is now experiencing a strong resurgence, however, due to the fact that there’s more clarity in relation to the outlook for businesses. Two stocks that are worth highlighting here are cloud computing company Snowflake and artificial intelligence firm Palantir. Both ended the month up more than 50% after posting better-than-expected earnings. Many other software stocks, including those of companies that specialise in work from home technology and cybersecurity solutions, outperformed as well.

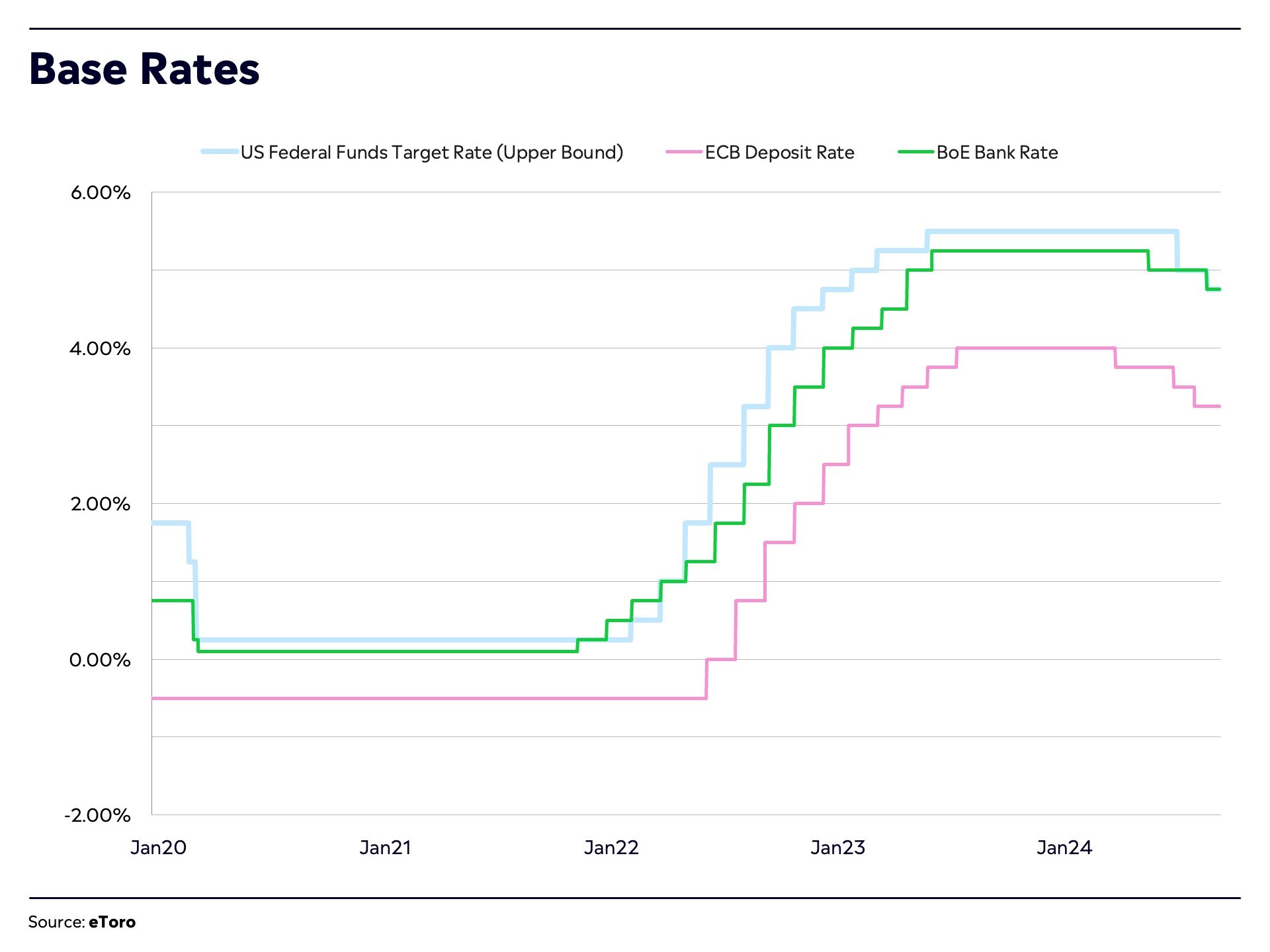

On the economic front, the US Federal Reserve cut interest rates by a quarter percentage point to a target range of 4.50%–4.75%. Meeting minutes showed that the central bank sees further rate cuts ahead but only “gradually.” In the UK, the Bank of England also cut rates by 0.25%, taking its base rate to 4.75%. It expects future cuts to be gradual as it believes that the new government’s first budget will lead to higher inflation and economic growth. In Europe, the next European Central Bank (ECB) meeting is scheduled for December 12 and economists currently expect a 50 basis point cut from the central bank. That would take its key deposit rate to 2.75%. As a result of interest rate differentials, the US dollar strengthened against the euro in November, hitting 0.96 at one point.

Turning to commodities, gold lost a little ground in November after beginning the month near all-time highs. It was hurt by a strengthening US dollar and rising bond yields. Oil experienced some ups and downs, but ended the period roughly flat. The conflict in the Middle East was a key driver of the volatility here.

For crypto investors, it was a phenomenal month, with Bitcoin rising as high as $99,000 on the back of the US election result. Donald Trump is pro-crypto and is likely to appoint a new US Securities and Exchange Commission (SEC) Chair who is crypto-friendly, leading to more relaxed regulation for the asset class. He has also vowed to create a national crypto reserve and support crypto miners. This has created a renewed sense of belief within the crypto markets, leading to strong gains for a range of assets including Ethereum, Cardano, and XRP.