Covering March Market

March was a turbulent month for stocks in which most major indexes lost some ground.

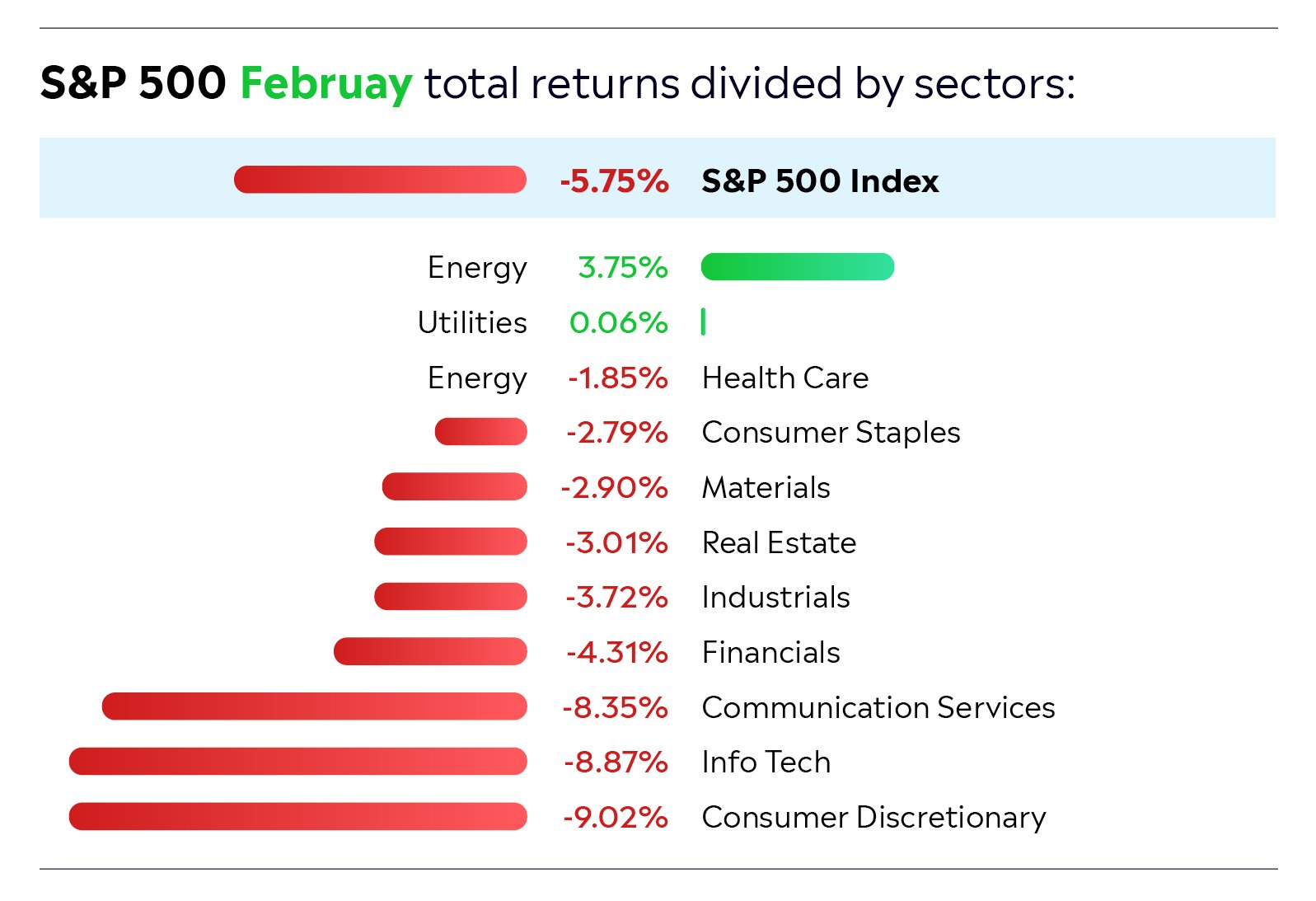

Tariff uncertainty, geopolitical issues, and recession/stagflation fears were the main drivers of the market weakness. For the period, the best-performing sector was Energy. Technology and Consumer Discretionary were the two worst-performing sectors.

US President Donald Trump’s tariffs dominated headlines in March, creating some significant volatility in the markets. Early in the month, markets were rattled after Trump announced tariffs on goods from a range of countries including Canada, China and Mexico (and saw retaliation from all of these countries). Late in the month, markets were shaken again after Trump announced 25% tariffs on the auto industry. At the end of March, investors were awaiting further updates on Trump’s tariffs (which were announced on April 2) and were in a “risk-off” mood.

It’s worth pointing out that Trump’s tariffs could have a range of effects.

On the one hand, they could encourage US consumers to buy American-made goods and protect industries in the country. On the other hand, they could potentially increase inflation and lead to lower growth globally. Note that during March, the Organization for Economic Co-operation and Development (OECD) reduced its forecast for global GDP growth in 2025 (from 3.3% to 3.1%) and in 2026 (from 3.3% to 3.0%) due to higher trade barriers in several G20 economies and increased policy uncertainty weighing on investment and household spending.

Another issue that was in focus in March — and had implications for the financial markets — was national security.

Early in the month, Trump paused US military assistance to Ukraine after a disastrous Oval Office meeting with Ukrainian President Volodymyr Zelenskyy in which Trump said Zelenskyy was “gambling with World War III.” Shortly after this, Trump cast doubt on his willingness to defend North Atlantic Treaty Organization (NATO) allies. NATO is a 75-year-old transatlantic alliance with a mutual assistance clause whereby an attack on one member is considered an attack on all.

On the back of all of these events, European countries scrambled to increase their defence budgets in an effort to bolster their national security and show Trump that they are capable of defending themselves. The UK, for example, announced that it would increase its defence budget from 2.3% of its GDP to 2.5% by 2027 — the biggest increase since the Cold War. Meanwhile, the European Commission announced a five-part plan to mobilise up to €800 billion in new defence spending over the next four years, declaring that Europe had entered an “era of rearmament.” This sent the value of European defence stocks such as Rheinmetall, Thales, and BAE Systems up sharply.

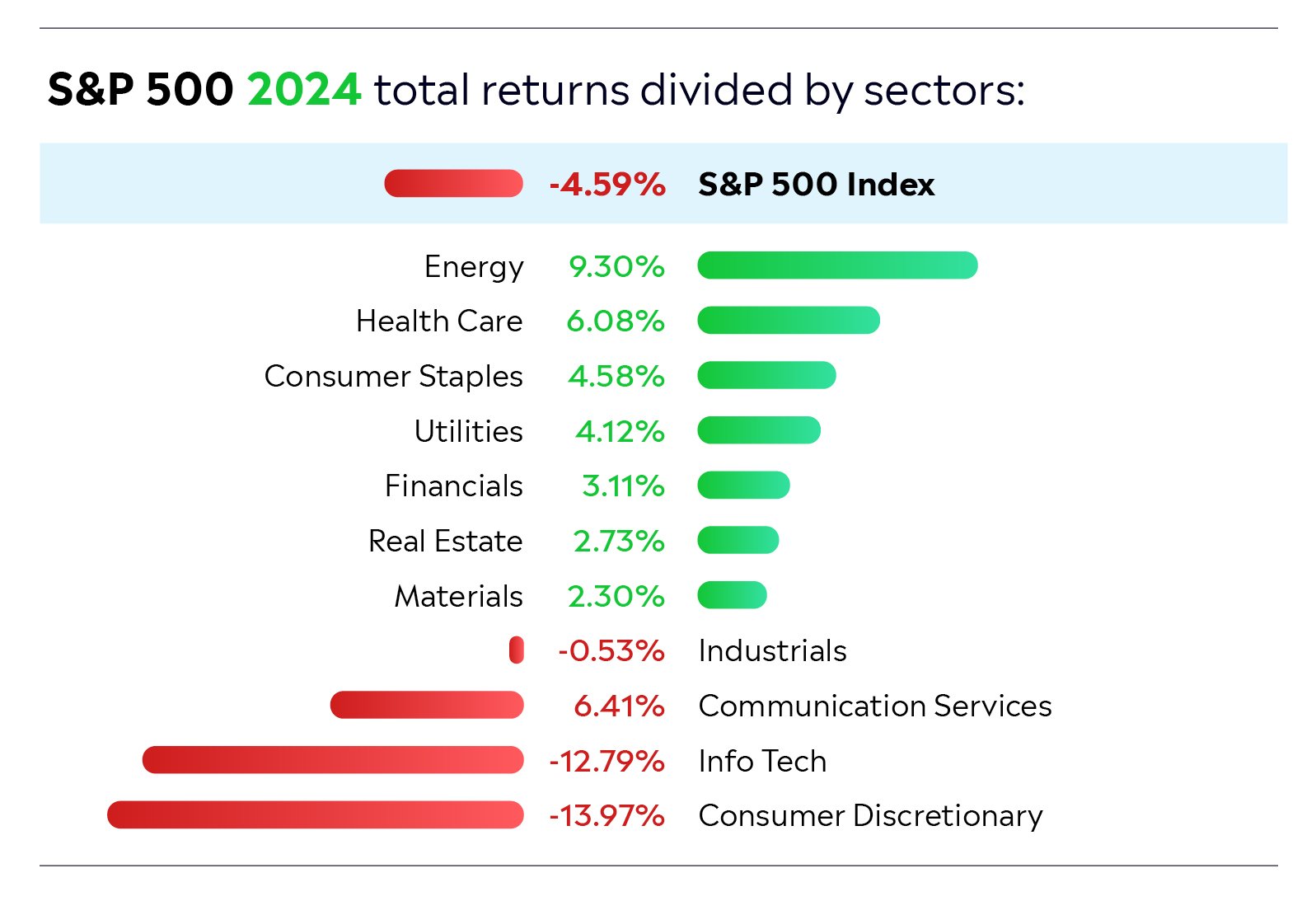

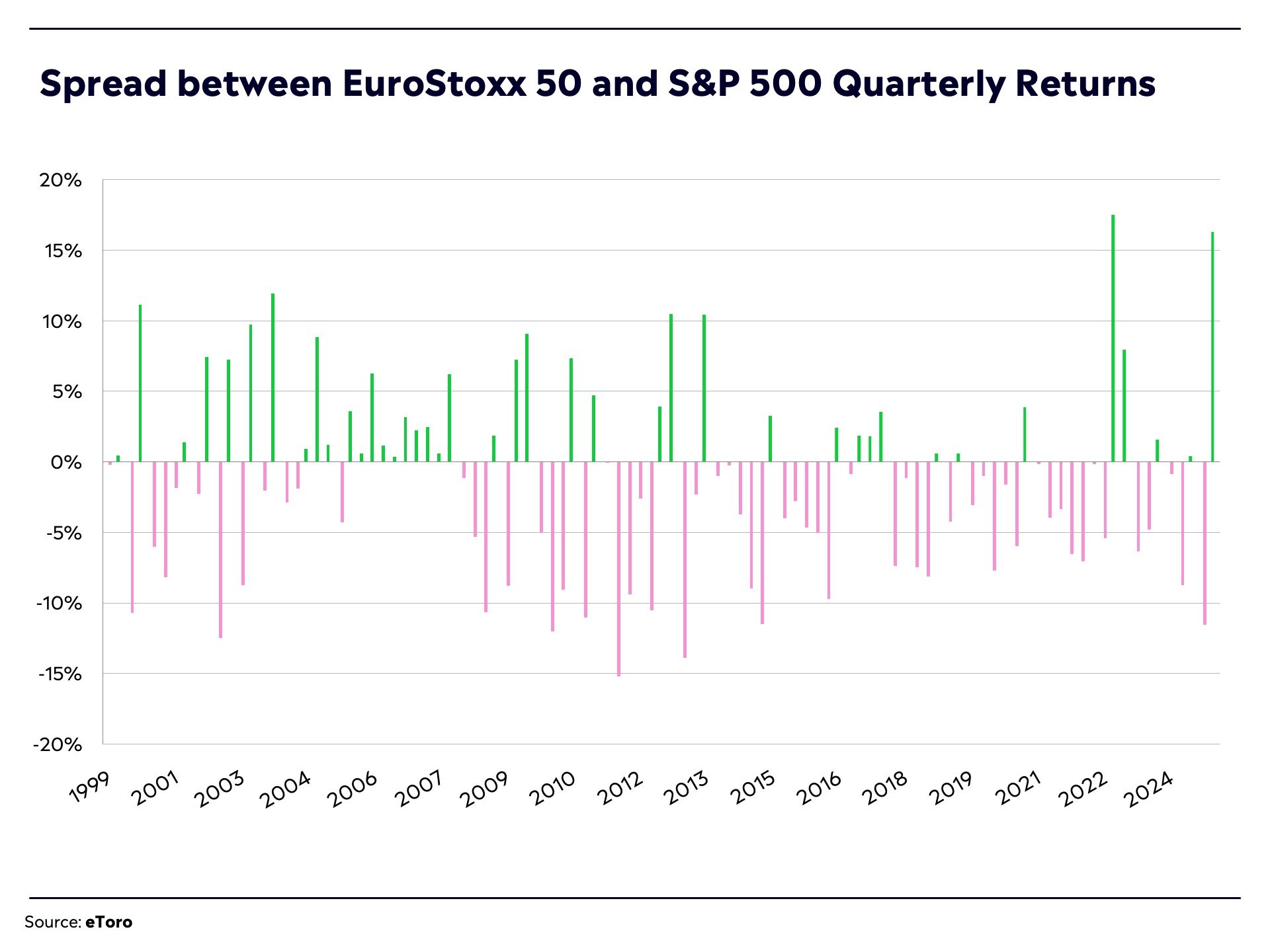

It’s worth noting that the strong performance by European defence stocks this year has boosted the European market substantially and has led to significant outperformance relative to US equities. While the S&P 500 closed March in negative territory (-4.59%) year-to-date, the Euro Stoxx 50 has returned 7.20%. One other factor that has led to outperformance from Europe is a move by institutional investors to diversify away from the US due to the high level of economic uncertainty. According to a survey of investors from BofA Global Research, March saw the biggest drop ever in the global allocation to US stocks.

Zooming in on the Magnificent 7, these stocks continued to underperform in March.

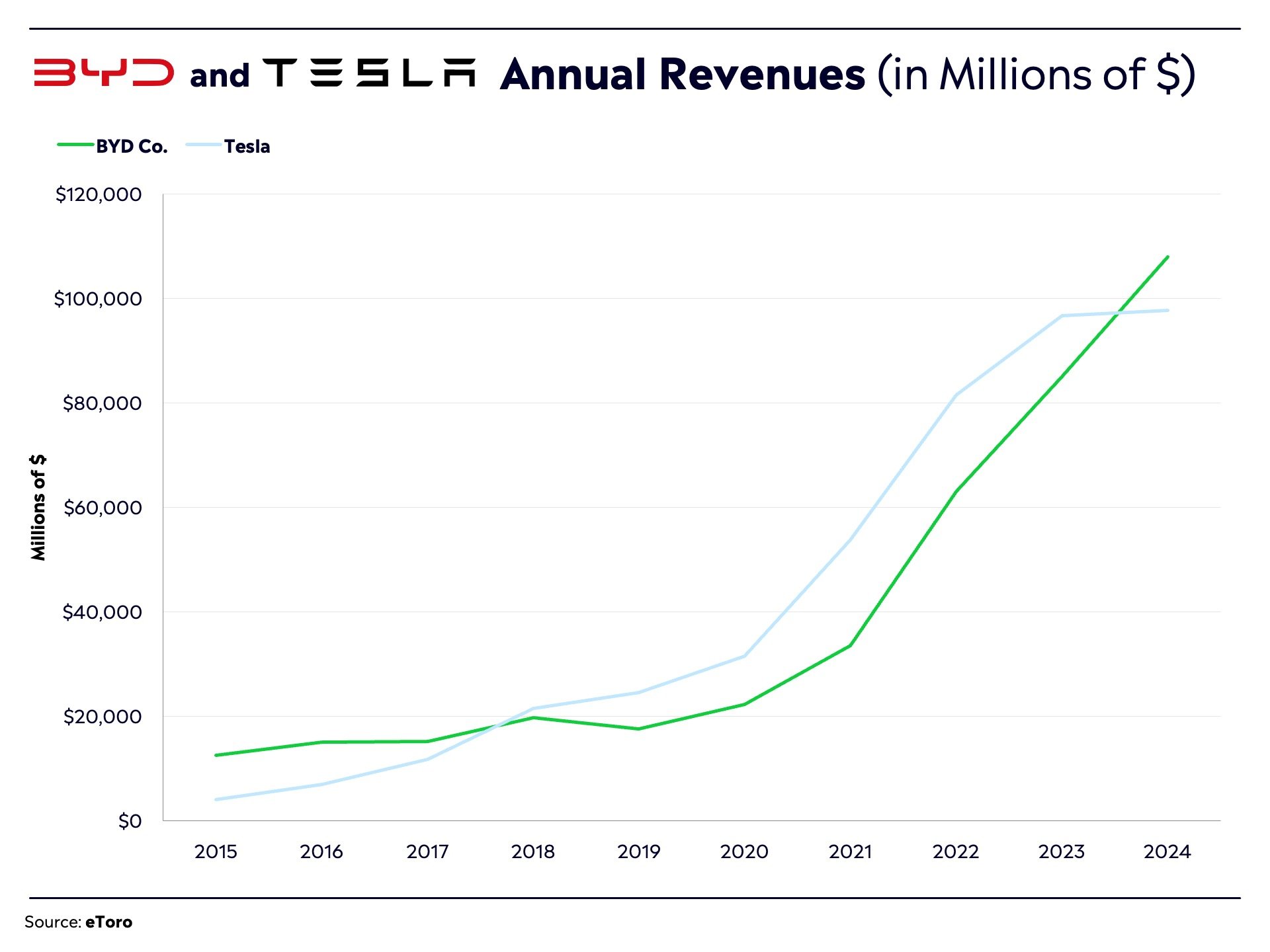

At one stage, Tesla fell as low as $217 per share — more than 50% below its recent high — since it was hurt by falling sales globally, concerns over competition from other EV companies such as BYD (BYD reached $100 billion in annual sales in 2024, surpassing Tesla’s $97 billion) and anger towards CEO Elon Musk. Other stocks such as Amazon, Apple, and Alphabet (the parent company of Google which bought cybersecurity company Wiz for $32 billion in March in one of the biggest tech acquisitions ever) also fell as investors lost interest in artificial intelligence (AI). For the first quarter of 2025, all Mag 7 stocks failed to produce gains for investors.

Speaking of AI, there was a lot of interest in CoreWeave’s IPO late in the month. CoreWeave is an AI infrastructure company that is backed by Nvidia. While the IPO was initially oversubscribed, it was downsized at the last minute, and shares closed flat at $40 on debut (putting the company’s market cap at $23 billion). This suggests that investor interest in AI has cooled for now.

Throughout the month, there was talk of a potential recession in the US.

One worrying indicator here was the University of Michigan’s Consumer Sentiment Index reading, which fell to its lowest level since early 2021 on concerns about higher prices and the economic outlook amid the Trump administration’s escalating tariffs. Another was the Conference Board’s measure of consumers’ short-term expectations, which dropped to its lowest level in 12 years. Worries over consumer spending resulted in weakness in economically sensitive areas of the market such as travel stocks.

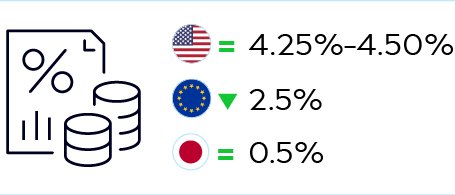

In terms of interest rates, the US Federal Reserve kept rates steady at 4.25%–4.50%, citing uncertainty around the economy and inflation. However, the European Central Bank (ECB) lowered rates — for the sixth time since June 2024 — to 2.5% (it indicated that its cutting phase may be nearing an end as inflation has cooled). In Japan, the Bank of Japan kept rates at 0.5%, despite being uncomfortable with inflation running at around 3%, citing uncertainty over the potential impact of US tariffs as the reason for not increasing rates. This led to Japan's 10-year government bond yield moving up to 1.52%, its highest level since 2009. It should be noted that many institutional investors borrow Japanese yen at low rates and invest the capital in higher-yielding assets (this is known as a “carry trade”). If rates in Japan were to keep rising, investors’ positions may need to be closed, creating further market volatility.

Turning to commodities, gold continued its strong run, hitting $3,000 per ounce for the first time ever and going on to climb above $3,100. On the back of this strength, gold miners produced positive returns. As for oil, it was relatively flat. In an interesting twist, copper jumped about 10% — normally copper underperforms if investors believe a recession is on the horizon.

Finally, crypto had an up-and-down month with Bitcoin ending the period at $82,000 after closing February at $84,000. During the month, the Trump administration signed an executive order to create a Bitcoin federal reserve with seized Bitcoin. However, investors had been expecting to see an active purchase of the cryptoasset by the US government. In Texas, the Senate passed a bill to form a state Bitcoin reserve in a move that signals growing interest in crypto.