Covering July Market

July was a mixed month for stocks with some areas of the market producing strong returns and others underperforming.

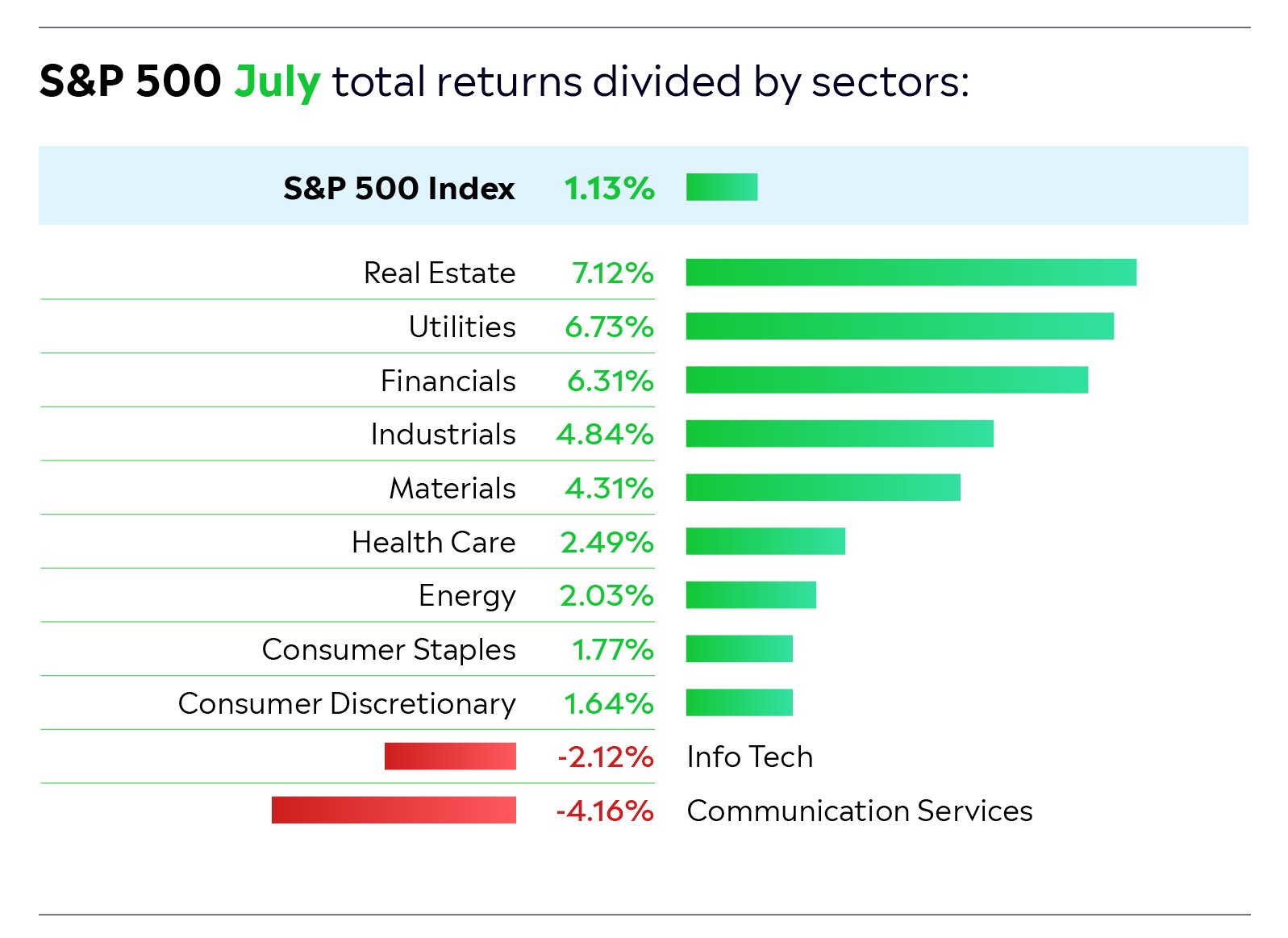

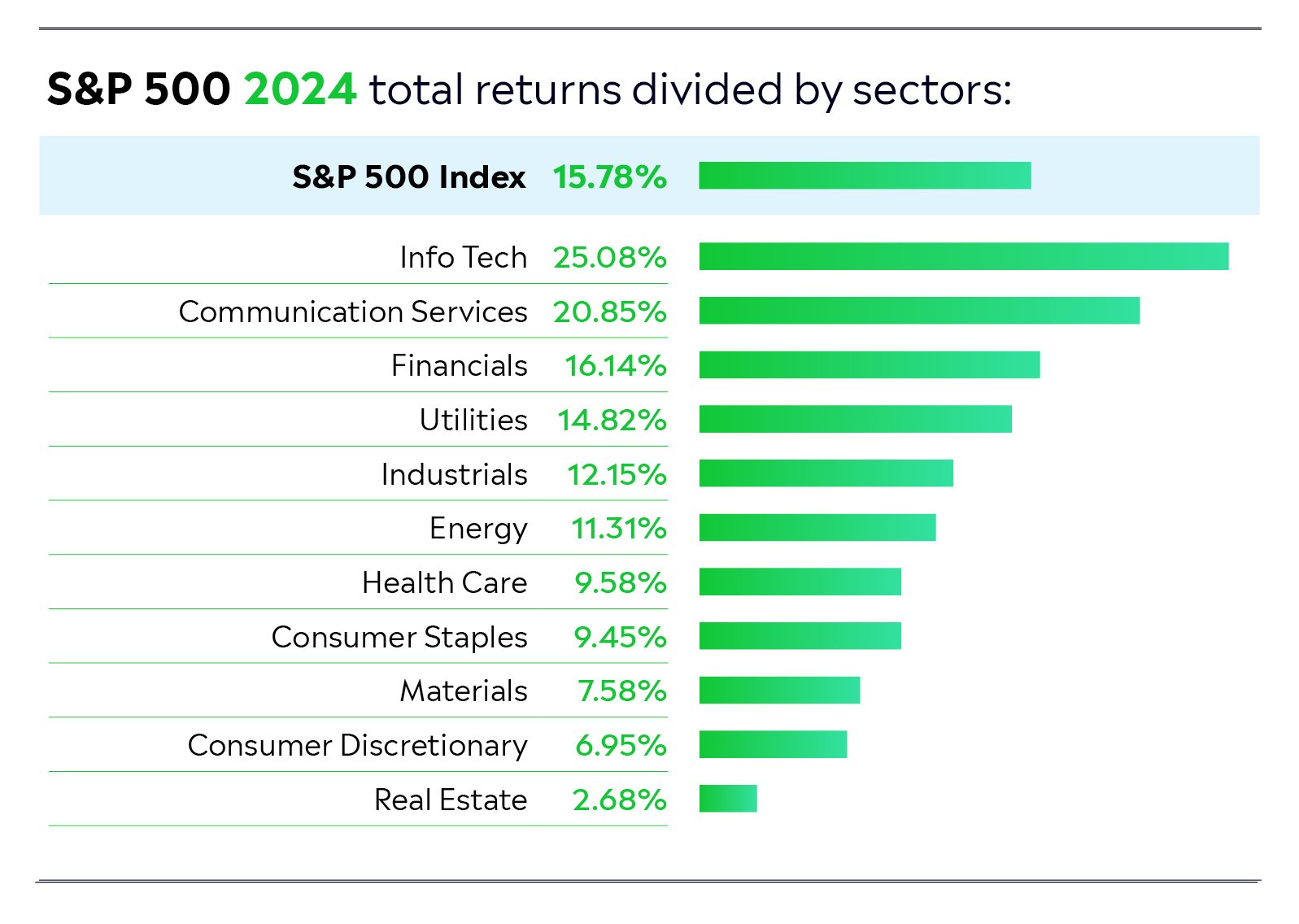

While major indexes such as the Nasdaq-100 and the Euro Stoxx 50 delivered underwhelming returns, small-cap stocks and real estate investment trusts generated significant gains. The best-performing sectors for the period were Financials and Real Estate, which benefitted from talk of interest rate cuts. Technology — which soared in H1 — was the biggest underperformer.

A key theme in July was a rotation out of Big Tech and artificial intelligence (AI) stocks into smaller companies.

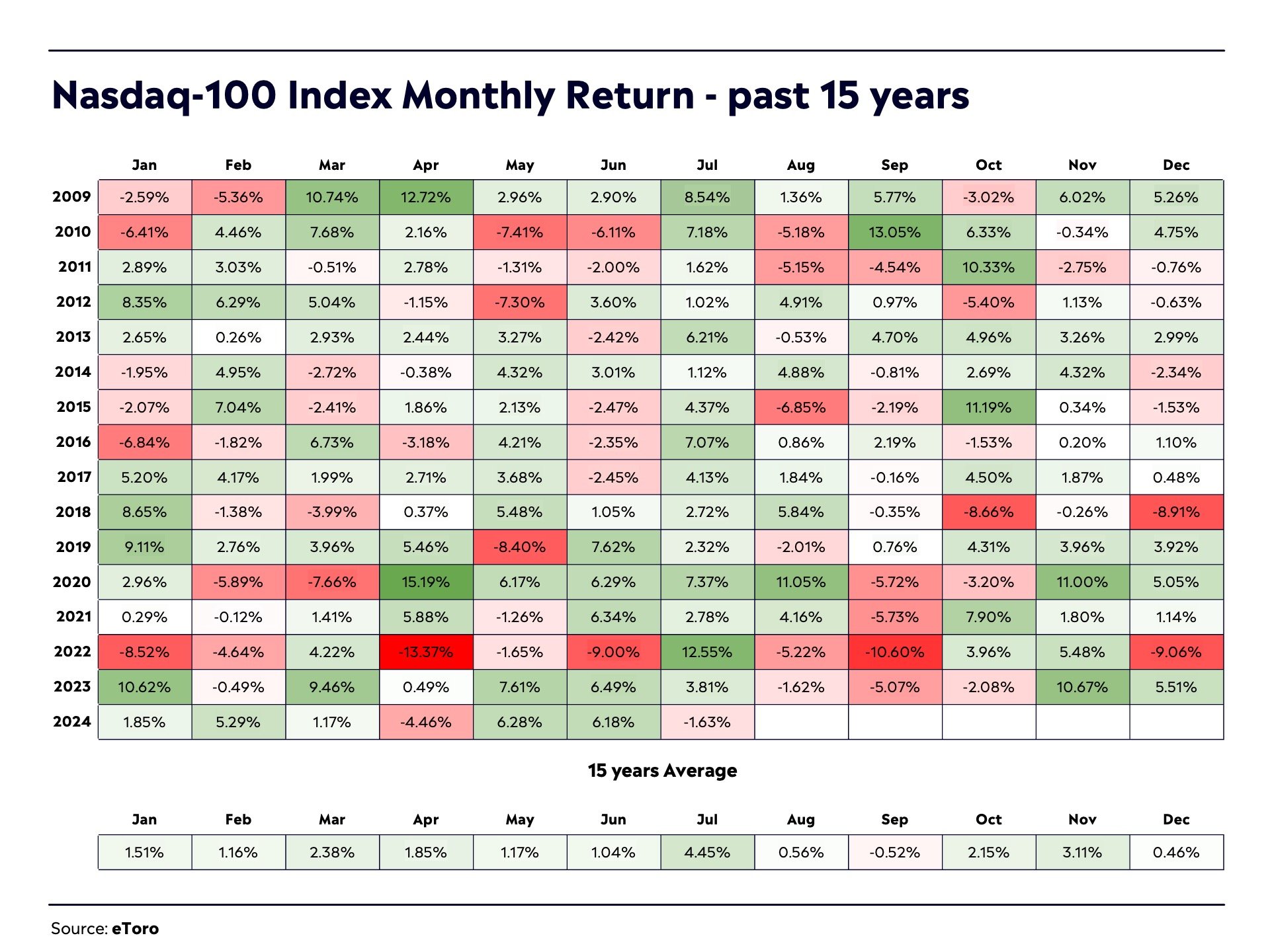

This shift — which saw the small-cap Russell 2000 Index post near double-digit gains for the month — was the result of several factors, including the outlook for interest rates (smaller companies are more sensitive to interest rates and so will benefit more from rate cuts), slightly underwhelming Big Tech earnings, and general profit-taking in the AI space. In H1, it was Big Tech, or the “Magnificent 7,” that was responsible for most of the market’s gains. However, it seems that many investors are now expecting the other 493 companies in the S&P 500 Index to lead the way. Late in the month, the tech-focused Nasdaq 100 Index fell 3.6% in a single day — its worst one-day performance since 2022. The index closed July in negative territory for the first time in 15 years.

Another major theme throughout the month was politics.

Early in July, the focus was on the UK election. This resulted in a landslide victory for Sir Keir Starmer’s Labour Party, ending the Conservatives’ 14-year period in power. Then came the French election. Here, France’s left-wing alliance, the New Popular Front won the most votes in the final round of voting, but failed to gain enough seats for a majority in the National Assembly, plunging France into uncertainty (there is no clear candidate for prime minister at present).

After these two events, attention turned to the US election, especially after US President Joe Biden announced that he was dropping out of the race and subsequently endorsed Vice President Kamala Harris. In the weeks leading up to this development, Donald Trump — who survived an assassination attempt in July — had been the clear favourite to be the next president. However, now, the chances of a Trump victory are far less certain (much will depend on the so-called “swing states,” which could potentially be won by either candidate). Throughout the month, there was considerable movement in assets that could potentially benefit or suffer from a Trump victory including crypto stocks (Trump is pro Bitcoin), electric vehicle (EV) stocks (Trump is a fan of old school combustion engine vehicles and wants to rescue the traditional US auto industry), and chip stocks (chip companies could face tighter export restrictions under Trump). Trump has a protectionist mindset and if he is elected as the next president, he would most likely attempt to tax foreign imports to increase the prices of these goods in the US. This “Trumponomics” move could increase inflation, keep interest rates higher, and favour the US dollar.

At stock level, Q2 earnings were in focus.

This resulted in some market volatility. Alphabet and Tesla were the first two Magnificent 7 companies to post their numbers which didn’t impress investors. While Alphabet beat revenues and earnings expectations, digital ad revenues from YouTube were below forecasts and capex guidance was higher than expected (due to AI spending). This led to share price weakness for the tech giant. Tesla also saw its share price fall after the company posted a decline in automotive revenues and pushed its much anticipated robo-taxi event back a few months. It’s worth noting, however, that before its Q2 earnings, Tesla stock had enjoyed an 11-day winning streak in which it gained more than 40%. Late in July, Microsoft posted its earnings and its numbers were solid, with overall revenue growth of 15%. Yet, the stock pulled back due to the fact that cloud growth of 29% was slightly below forecasts (30-31%). Chip company AMD also posted its earnings late in the month. Its share price jumped after the company reported strong demand for its AI chips.

In the cybersecurity space, CrowdStrike shares took a big hit after the company was responsible for a major IT outage that affected banks, airlines, hospitals, and payment systems around the globe. One of the largest IT outages in history, it was caused by a software update that crashed Microsoft Windows’ operating system. It is estimated that the crash is going to cost firms billions of dollars. Delta Airlines — which was badly affected by the outage — has hired lawyers and plans to seek compensation from CrowdStrike.

Also, in the cybersecurity arena, Alphabet made a $23 billion offer for cloud security software company Wiz. The deal was rejected by Wiz, however, as it wants to remain independent for now (and potentially do an IPO at some stage). If the deal had gone through, it would have been Alphabet’s largest acquisition ever. This suggests that Alphabet believes that cybersecurity is an area of technology with strategic importance.

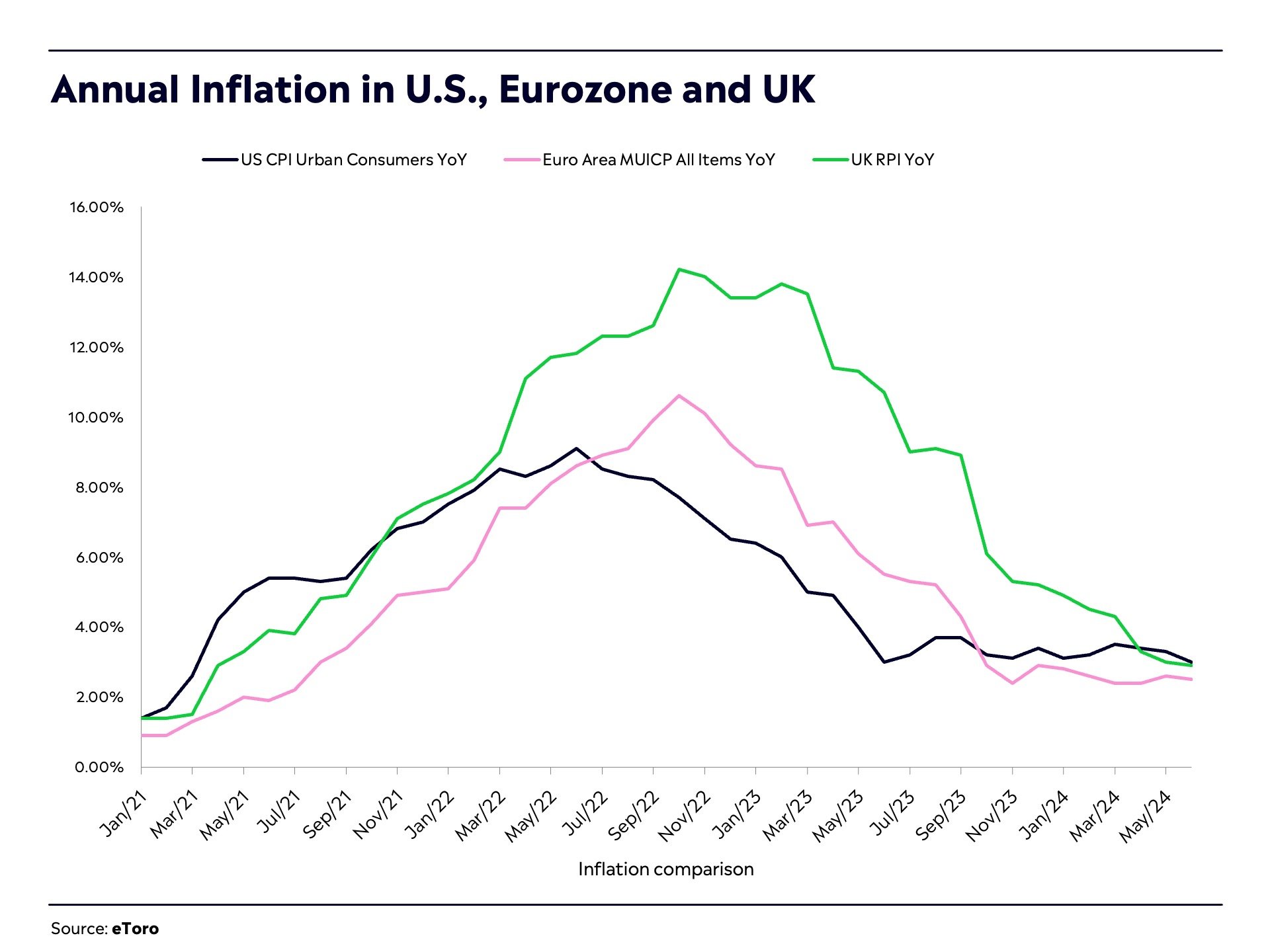

On the economic front, data showed that the US economy grew at an annualised rate of 2.8% in the second quarter of 2024 (double the rate in Q1), capping two years of solid expansion. However, a jobs report in July showed a slowdown in the labour market, with unemployment rising above 4% for the first time in two years. Given the labour market data, and cooling inflation (US CPI inflation came in at 3% in June — its lowest level in more than three years), most economists are expecting a rate cut from the Fed in September. Many experts are starting to think that the central bank will cut rates twice this year now.

In China, The People’s Bank of China (PBOC) surprised investors by unexpectedly lowering the rate on its one-year medium-term lending facility. This is the rate that the central bank charges to lend money to commercial banks for 12 months. The cut from 2.5% to 2.3% — the largest since April 2020 — came following a surprise reduction to a key short-term policy rate. So, clearly the PBOC is willing to make some big moves to support the Chinese economy. Elsewhere in Asia, the Bank of Japan (BoJ) raised its benchmark interest rate to 0.25% from a range of 0% to 0.1%. This led to a huge rally for the Japanese yen, which finished July near a rate of 150 to the US dollar after falling to 161 at one stage during the month (the lowest level since 1986).

Turning to commodities, gold hit a record high in July, crossing $2,480 per ounce, before a pullback in the second half of the month. Gold is up more than 18% year-to-date, supported by large purchases from central banks, strong consumer appetite in China, demand for safe-haven assets amid geopolitical tension and political uncertainty, and hopes of rate cuts (you can find more information on gold in the trends section of this report). Oil prices weakened in July amid concerns over demand in a slowing economy. However, it’s worth pointing out that Trump’s Vice President choice J.D. Vance is a staunch supporter of the oil industry and an opponent of renewable energy.

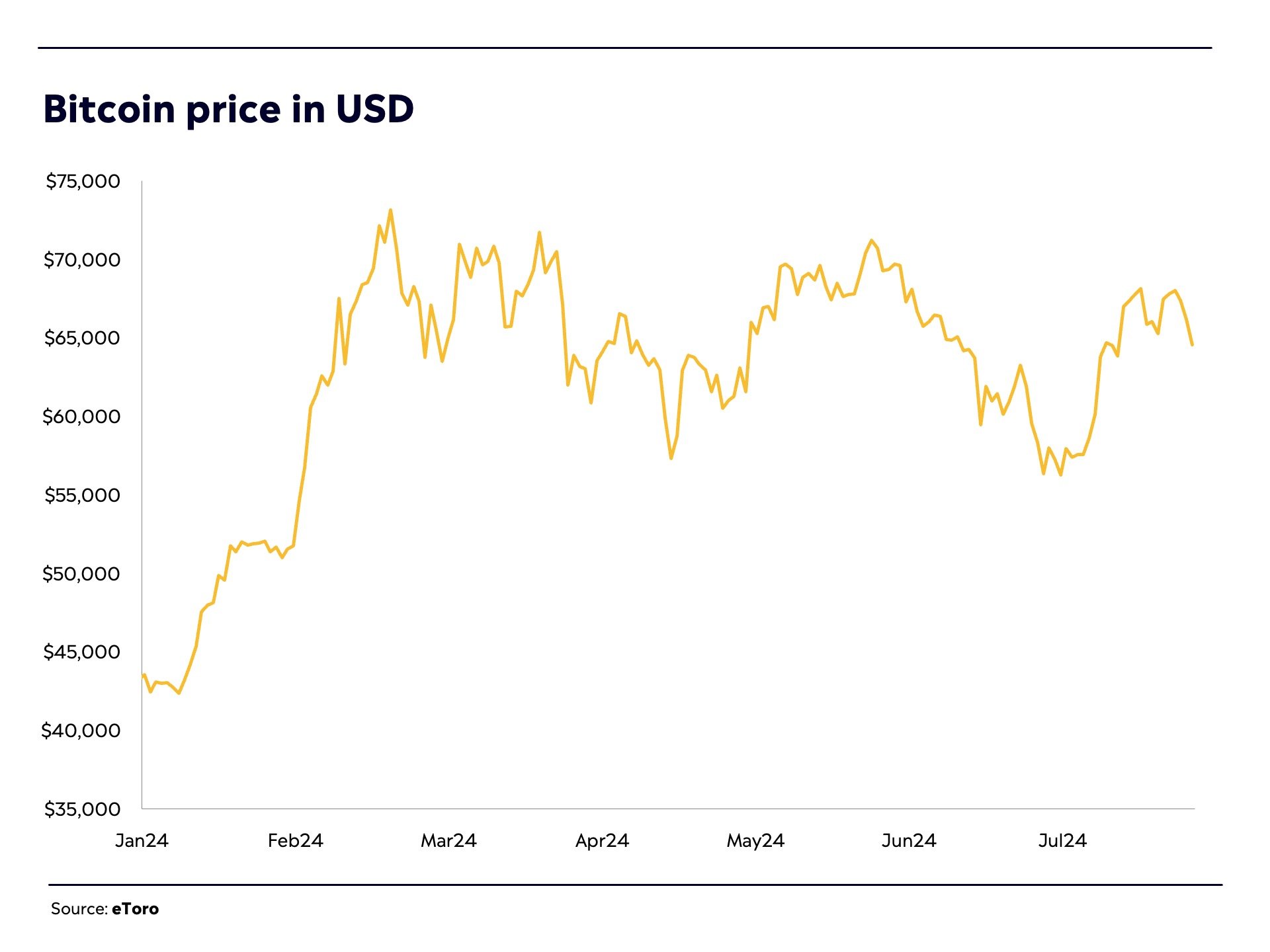

As for crypto, it was a volatile month for the asset class, with both Bitcoin and Ethereum rising significantly after a pullback early on. The strength here was the result of a pro-Bitcoin speech by Donald Trump and expectations of US rate cuts. The cryptos ended the month nearly unchanged.