In the Spotlight Trends of the Month

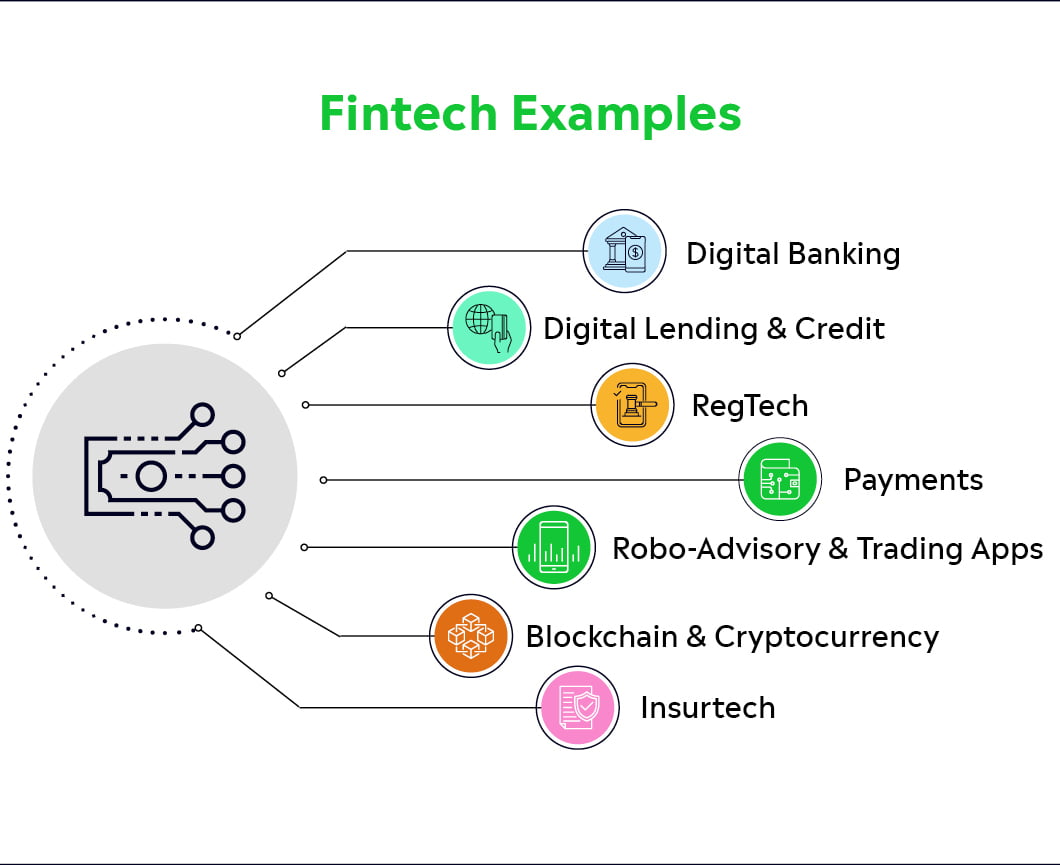

FinTech (financial technology) is one of the fastest-growing areas of technology today. An innovative, dynamic industry, it is disrupting a wide range of business models including banking, payments, and insurance.

Within fintech, there are a number of different sub-sectors. With that in mind, here’s a look at three key areas of financial technology and some companies that have been making moves lately.

Currently, it accounts for more than 80% of global revenues. One company in this area of the market that has made headlines this year is PayPal. Recently, it introduced a “tap-to-pay” feature for US merchants using the Venmo and Zettle (PayPal’s flexible point-of-sale (POS) system) apps on Android phones. This is a big deal as it means that small businesses in the US can now accept contactless payments from cards and digital wallets directly on their mobile devices without the need for additional hardware.

PayPal also just launched a Venmo Teen Account, which allows parents to open accounts for children aged 13 to 17. This could turn out to be a savvy move, as there are an estimated 25 million potential new customers in this age group and capturing these consumers at a young age could lead to long-term revenue for the company. Meanwhile, on the buy now, pay later (BNPL) front, PayPal recently agreed to sell up to €40 billion worth of European Pay Later Receivables to private equity firm KKR. This is expected to generate about $1.8 billion in gross proceeds and PayPal plans to use a large chunk of this money for share buybacks.

Outside the US, European PayTech Nexi recently announced that it had signed an agreement with energy company Eni to offer innovative electronic payment services for Eni and its companies across Europe. The partnership could potentially help Eni to improve the payments experience for its customers. It could also help the energy giant take advantage of future opportunities arising from the evolution of payment systems.

Today, new digital banks or “neobanks” are springing up everywhere and capturing market share from the traditional banks. These banks — which have slick apps that have been built for the digital age — don’t have physical branches like traditional banks. As a result, they can offer consumers lower fees and more competitive interest rates.

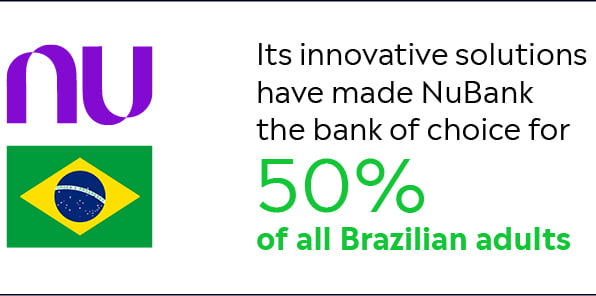

One neobank that has a lot of momentum right now is Brazil's NuBank, which is owned by Nu Holdings. The largest fintech in Latin America, it has gained more than 85 million customers since its launch in 2013. Incredibly, half of all adults in Brazil are customers of the bank today. How has the digital bank managed to capture so many customers across Brazil? Well, a lot of it has to do with its superior offering. In the past, the Brazilian banking system was known for its high fees and a lack of technology. When NuBank arrived on the scene, it offered an innovative solution, and as a result, it was able to capture significant market share. Other neobanks enjoying success include Green Dot, which has opened nearly 70 million accounts across the US to date, and SoFi, which offers a broad range of lending and wealth management services.

This is technology that aims to improve lending processes. Here, peer-to-peer (P2P) companies are having a lot of success, which is not particularly surprising given that they remove intermediaries from the lending process. One company in this space that is doing well right now is LendingClub, which operates a marketplace of loans. It has a smart business model in that it receives a fee from every loan taken but incurs no credit risks. So, it has much cheaper operations than the banks, which face credit risks. It’s worth noting that LendingClub saw its deposits rise by around 13% in the first quarter of 2023 amid the recent regional banking crisis.

Those interested in gaining exposure to the fast-growing fintech industry may wish to check out eToro’s new Fin-Tech Smart Portfolio. This is a diversified investment portfolio that provides access to a wide range of global fintech companies, including payments organisations, digital banking businesses, InsurTechs, financial market infrastructure companies, and more.

Yes, I am already investing in FinTech companies

Yes, I am interested in investing in FinTech companies. (@Fin-Tech)

Unsure or need more information about investing in FinTech.(learn more)

No, I am not interested in investing in FinTech companies.

Traditional finance (TradFi) refers to traditional, centralised financial systems that are based around institutions such as banks, insurance companies, and regulatory bodies. Decentralised finance (DeFi), on the other hand, is an emerging financial framework based on blockchain technology, which aims to create open, permissionless financial services without intermediaries. In the years ahead, the convergence of TradFi and DeFi is likely to create a powerful financial system with the stability of traditional finance and the innovation of decentralised finance. This should lead to enhanced financial products and services, innovation, and more inclusivity.

In recent months, we’ve seen a number of game-changing developments in relation to the merging of TradFi and DeFi.

For example, in June, investment management powerhouse BlackRock filed an application with the US Securities and Exchange Commission (SEC) for a Bitcoin exchange-traded fund (ETF). This will allow investors to gain exposure to Bitcoin’s price movements without owning the cryptoasset directly.

Meanwhile, in July, ETF specialist WisdomTree (which also plans to launch a Bitcoin ETF) launched a digital asset-based financial services mobile app. Called WisdomTree Prime, this app allows users to save, spend, and invest in cryptoassets such as Bitcoin and Ethereum, blockchain-enabled funds, and tokenised versions of physical assets such as gold. The aim of the app is to give consumers a secure, transparent, and easy-to-use way to spend, save, and invest their money.

Another major development was the launch of EDX Markets — a revolutionary crypto trading platform designed for institutional investors. This platform, which has been backed by industry giants such as Charles Schwab, Fidelity, and Citadel Securities, is a testament to the sustained institutional interest in the crypto market. It has already commenced trading for major cryptoassets such as Bitcoin, Ethereum, and Litecoin.

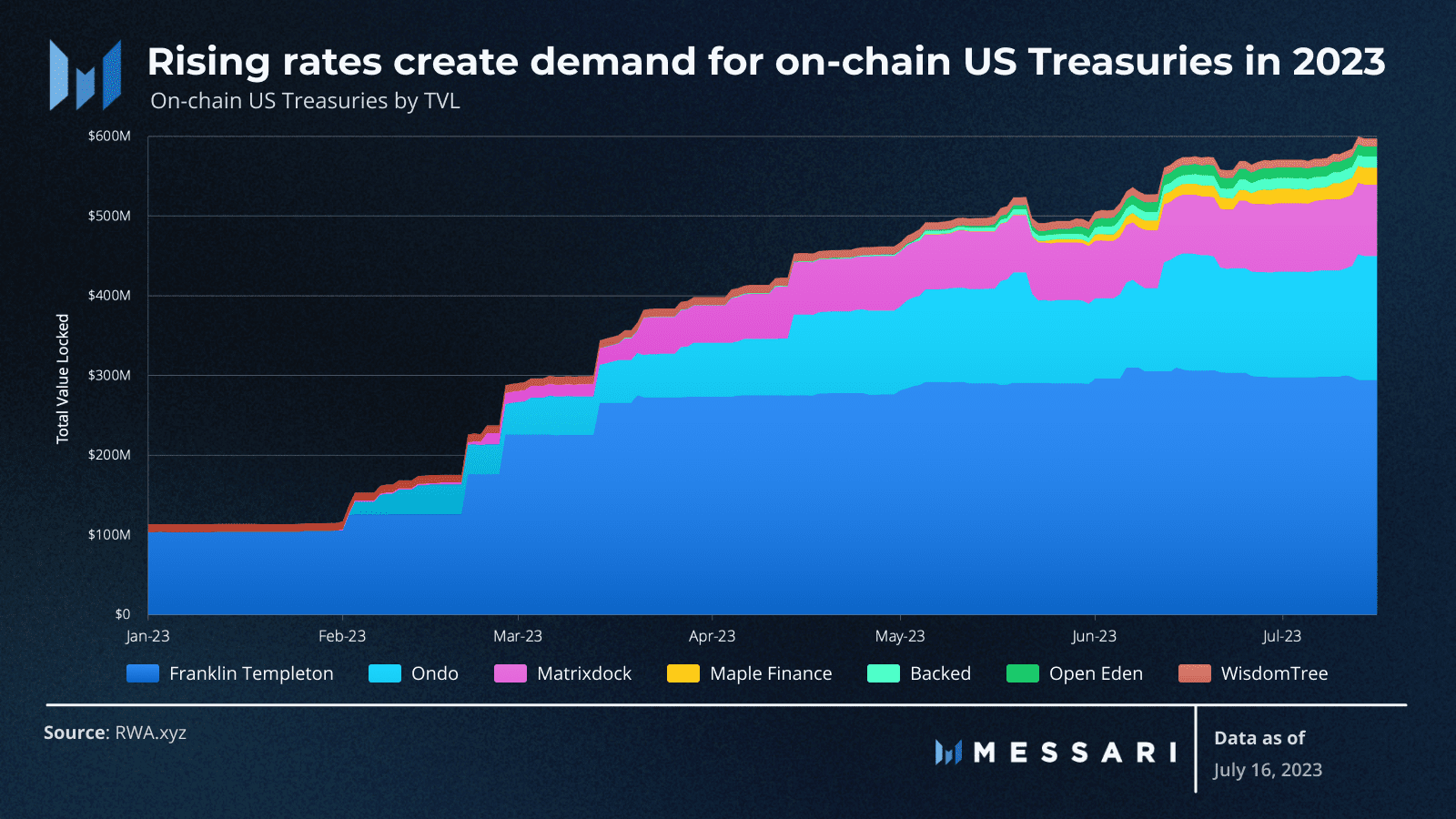

There has also been significant interest in tokenised US Treasuries in 2023. This is due to the fact that recently, bond yields have surpassed rates in DeFi lending markets. One company that is active in this space is Ondo Finance. It recently issued a tokenised version of BlackRock’s short-term US government bond ETF natively on Polygon as part of a strategic alliance.

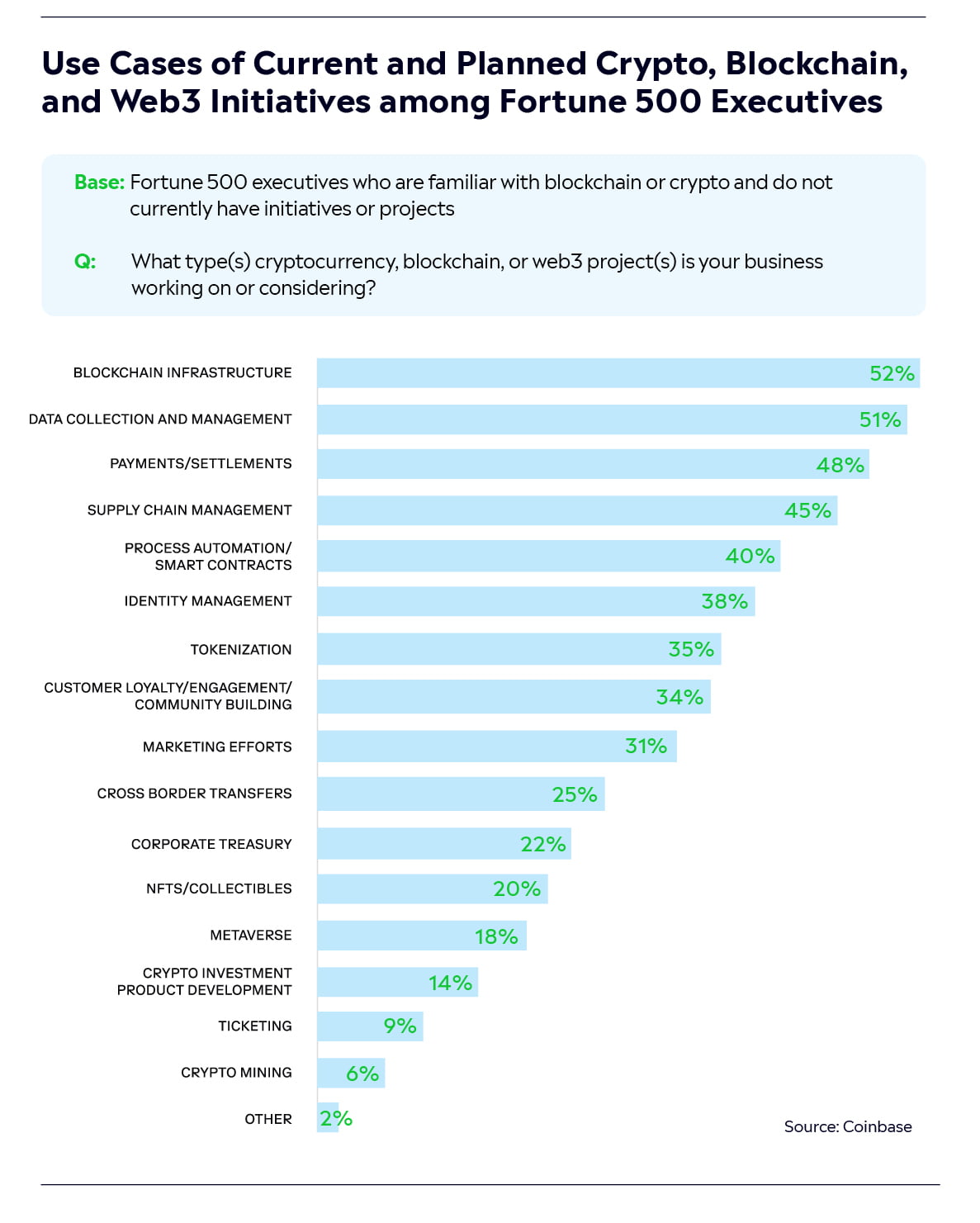

Looking ahead, we’re likely to continue seeing major corporations embrace the world of DeFi. According to research by Coinbase, nearly two thirds (64%) of Fortune 500 executives who are familiar with cryptoassets/blockchain say that investing in these technologies is important in order to stay ahead of the competition and that Web3 technologies will be pivotal for business. Many see this technology as similar to the Internet or artificial intelligence (AI).

The growing interest in merging TradFi and DeFi stems from several key factors, including:

Innovation and efficiency DeFi's innovative solutions offer speed and accessibility and merging TradFi with DeFi will lead to new, superior financial services.

Financial inclusionDeFi enables those who are unbanked to have access to financial services. In 2021, a World Bank report showed that in developing countries, just 20% of adults receive their salary into a bank account.

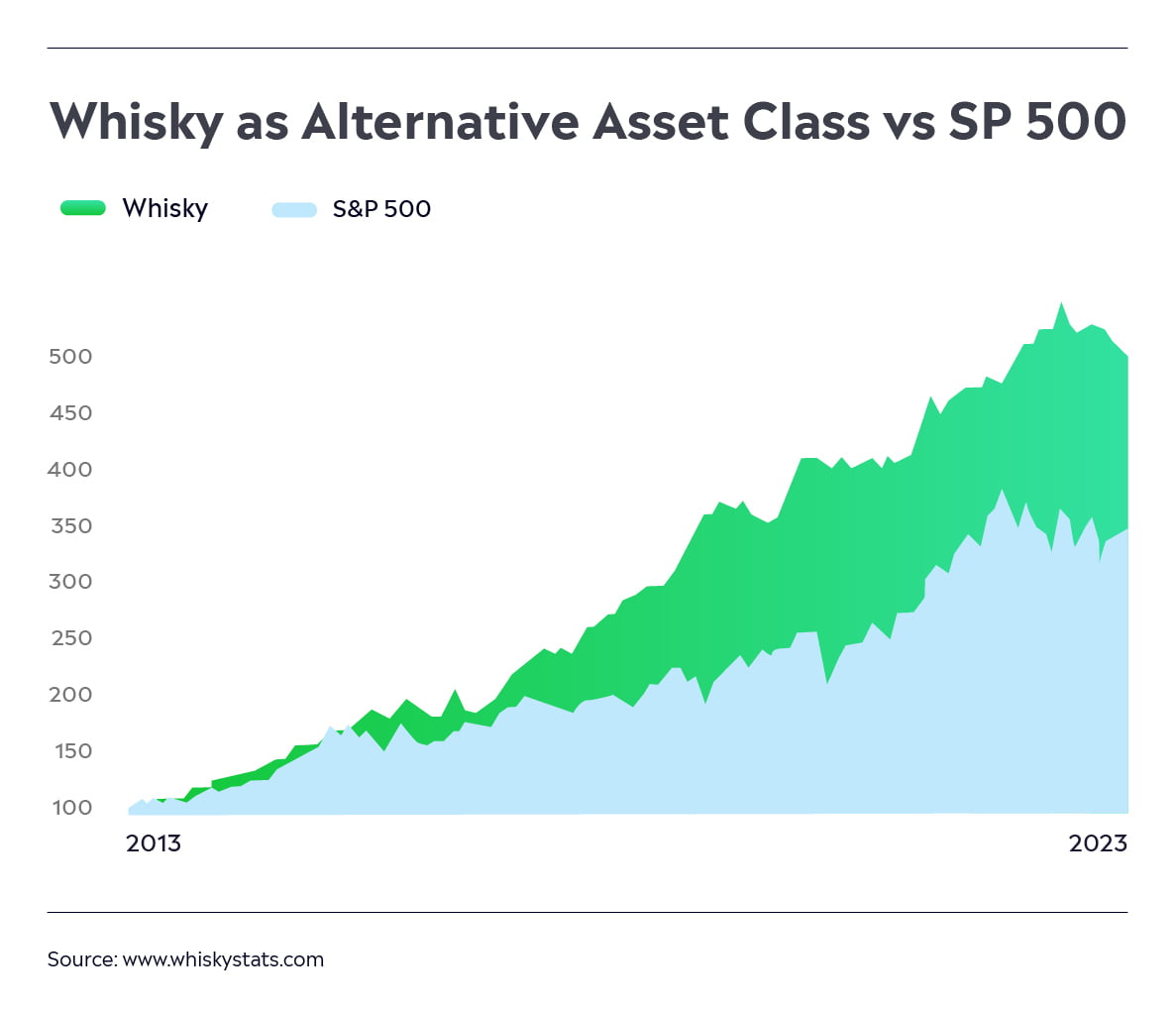

Real-world asset tokenisationBy tokenising assets, we can significantly increase global investment opportunities. Advantages of tokenisation include the potential to invest in traditionally illiquid assets (e.g., fine art, whisky, vintage cars, etc.), fractional ownership, enhanced transparency, and 24/7 market access.

Regulatory framework developmentMerging TradFi and DeFi fosters the development of regulatory frameworks and ensures compliance and investor protection.

Of course, while the convergence brings together expertise, resources, and innovation from both worlds, there are some barriers that need to be overcome to reach mass adoption. These include:

Regulatory challengesThe differing regulatory frameworks for TradFi and DeFi pose a barrier to their merger. What’s needed is the establishment of regulations that address the unique characteristics of decentralised finance.

Scalability and efficiency issuesDeFi protocols need to enhance scalability and efficiency so that they can handle larger transaction volumes comparable to those in TradFi.

Standardisation and integration Bridging the technological gap between TradFi and DeFi requires the development of common standards and protocols to enable seamless communication and asset transfer. It also requires the integration of decentralised technologies in the legacy systems of TradFi.

Market perceptionBuilding trust, and demonstrating the benefits and viability of merging TradFi and DeFi, are essential to overcoming hesitations and gaining wider market adoption by traditional financial institutions.

Yet, with institutions recognising the potential of DeFi, regulatory frameworks evolving, and ongoing technological advancements, the merging of TradFi and DeFi is set to continue. In the process, it should reshape the financial landscape and create a more integrated, efficient, and inclusive financial ecosystem.

Those interested in positioning their portfolios for the convergence of TradFi and DeFi may wish to consider eToro’s DeFiPortfolio Smart Portfolio, which provides access to a range of cryptoassets that are active in the DeFi space, the Web3Applications Smart Portfolio, which offers access to a range of decentralised application (dApp) projects at the heart of the Web3 revolution, or alternatively, crypto-focused Smart Portfolios such as CryptoEqual, Crypto-currency, and CryptoPortfolio.