Covering July Market

Stocks made an excellent start to the second half of 2023, with all major indexes posting solid gains in July.

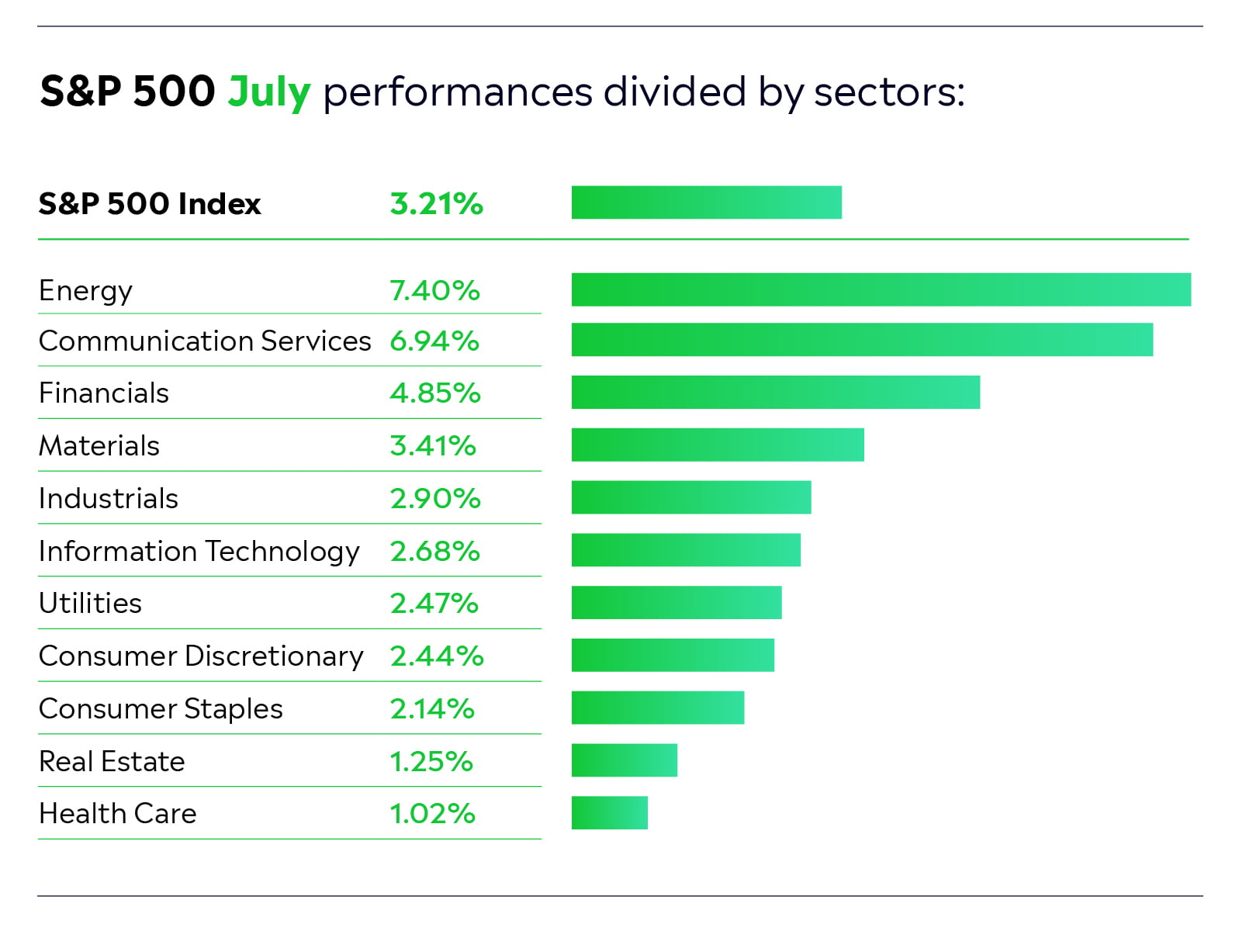

The best-performing sector was Energy, which rallied amid signs that the US may be able to avoid a recession, and helped the Dow Jones post a historic 13 consecutive up days. Communication Services also did well — thanks to strong earnings from Meta Platforms and Alphabet. More defensive sectors, such as Healthcare and Consumer Staples, which have underperformed this year, continued to lag.

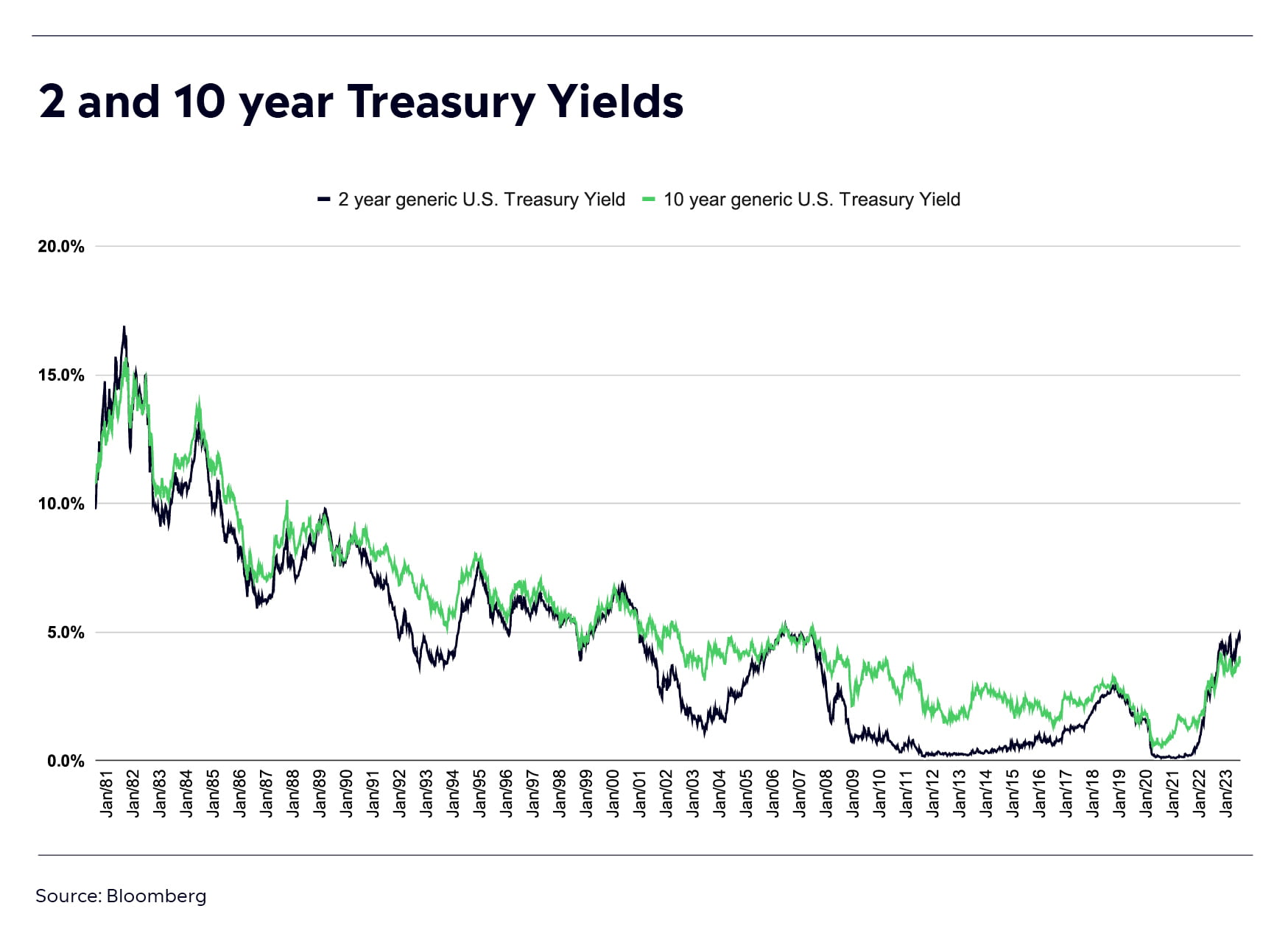

Early in the month, stocks were rocked by a strong US jobs report and a hawkish Federal Reserve. After minutes from the Fed’s June meeting revealed an intent to continue increasing interest rates, 2-year Treasury yields surpassed the 5% level, hitting levels not seen since 2007. Meanwhile, 10-year Treasury yields rose above 4%. These yields unsettled equity market investors.

However, in the middle of the month, sentiment towards stocks improved after US CPI inflation came in at 3.0% — the lowest rate since March 2021. This reading was lower than expected, offering fresh hope that the Fed will soon conclude its interest rate increases. Late in the month, the Fed made a 0.25% rate hike, taking the Fed funds rate to a target range of 5.25%–5.5% (the highest level in more than 22 years). However, this small rate hike was largely anticipated and didn’t spook investors. Looking ahead, Fed Chair Jerome Powell said that the central bank will make data-driven decisions on a “meeting-by-meeting” basis. Yet, many economists believe that we may have seen the last rate hike for a while.

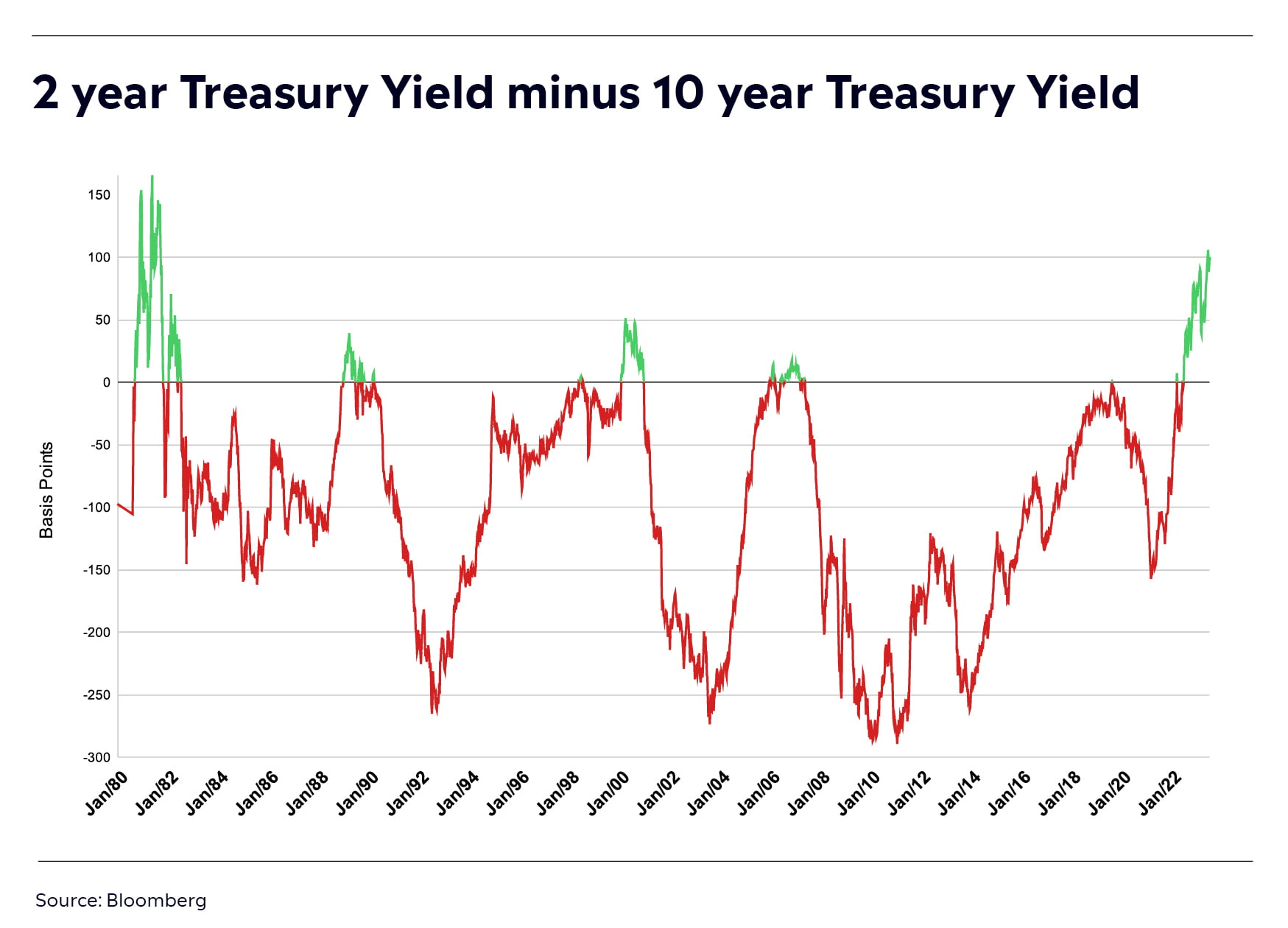

It’s worth noting that the US yield curve remained inverted in July and that the spread between 2-year Treasury yields and 10-year Treasury yields reached 108 basis points — the largest spread in 42 years. An inverted yield curve is a classic signal that a recession is on the horizon. Since 1978, the yield curve has inverted six times (not including the current inversion) and has preceded a recession on each occasion. So, a recession could still be on the cards.That said, some experts think that the current yield curve inversion may be sending out a false signal.

Outside the US, inflation in the UK cooled more than expected in a sign that high interest rates may be starting to curtail the worst wage-price spiral in the G7. UK CPI came in at 7.9% for June, lower than the previous 8.7% print in May. This led market analysts and investors to cut estimates of further interest rate hikes from the Bank of England (BoE) and weaken the British pound slightly. Earlier in the month, the pound had hit 1.31 against the US dollar — a 15-month high. The European Central Bank (ECB) increased rates by another 0.5% — its ninth consecutive hike — but raised the possibility of a pause in September.

In Japan, Tokyo CPI came in at 3.2% for July versus the consensus forecast of 2.8%. This led the Bank of Japan (BoJ) to loosen its yield curve control and announce that it would have “greater flexibility” in its monetary policy going forward. This sent shock waves throughout the world’s financial markets as the central bank has used yield curve control to manage interest rates since September 2016. The BoJ left its short-term policy interest rate unchanged at -0.1%.

In China, producer prices fell 5.4% year-on-year in June — the largest rate of decline since December 2015 — underscoring the economic challenges that the world’s second-largest economy is facing right now. As a result, the government pledged to step up support for the economy, and further ease policy curbs in the property sector.

In the second half of the month, the focus was largely on corporate earnings. Banks got the ball rolling as usual, and results here were generally good, with JP Morgan, Bank of America, Citigroup, Wells Fargo, and Morgan Stanley all posting better-than-expected earnings.

In the tech space, earnings were mixed. Meta Platforms — which launched “Threads” during the month in an effort to take on Twitter (which is now known as “X”) — saw its share price rise to the highest level since January 2022 after it revealed that artificial intelligence is helping the company boost engagement and ad sales on its social media platforms. Meanwhile, Alphabet stock popped after revenue from Google ads, YouTube ads, and Google Cloud all beat forecasts.

On the downside, Netflix stock fell after the company narrowly missed revenue forecasts, while Tesla shares declined after the company revealed a drop in profit margins (Tesla still ended the month higher). Semiconductor results varied — NXP Semiconductors, which is a big player in the autonomous driving space, and Lam Research, which makes chip manufacturing equipment, both did well, while Taiwan Semiconductor Manufacturing Company cut its outlook despite strong demand for AI chips.

During July, there was some encouraging news on the M&A front. The $69 billion deal between Microsoft and video game company Activision Blizzard looks like it may actually go through now after the US Federal Trade Commission (FTC) withdrew its case against the deal and the UK’s Competition and Markets Authority (CMA) said that it is ready to negotiate. As for Broadcom’s $61 billion deal for cloud computing company VMware, it won conditional EU antitrust approval during the month.

In the commodities space, it was a good month for oil, which hit three-month highs on the back of tightening supplies. The pledges from Chinese leaders to step up economic support for the country also improved sentiment. Gold performed well too, thanks to a weaker US dollar and a dip in US Treasury yields.

As for crypto, it was generally a flat month with Bitcoin and Ethereum trading sideways. XRP surged higher, however, after a US judge ruled that Ripple’s sales of XRP tokens were not investment contracts.