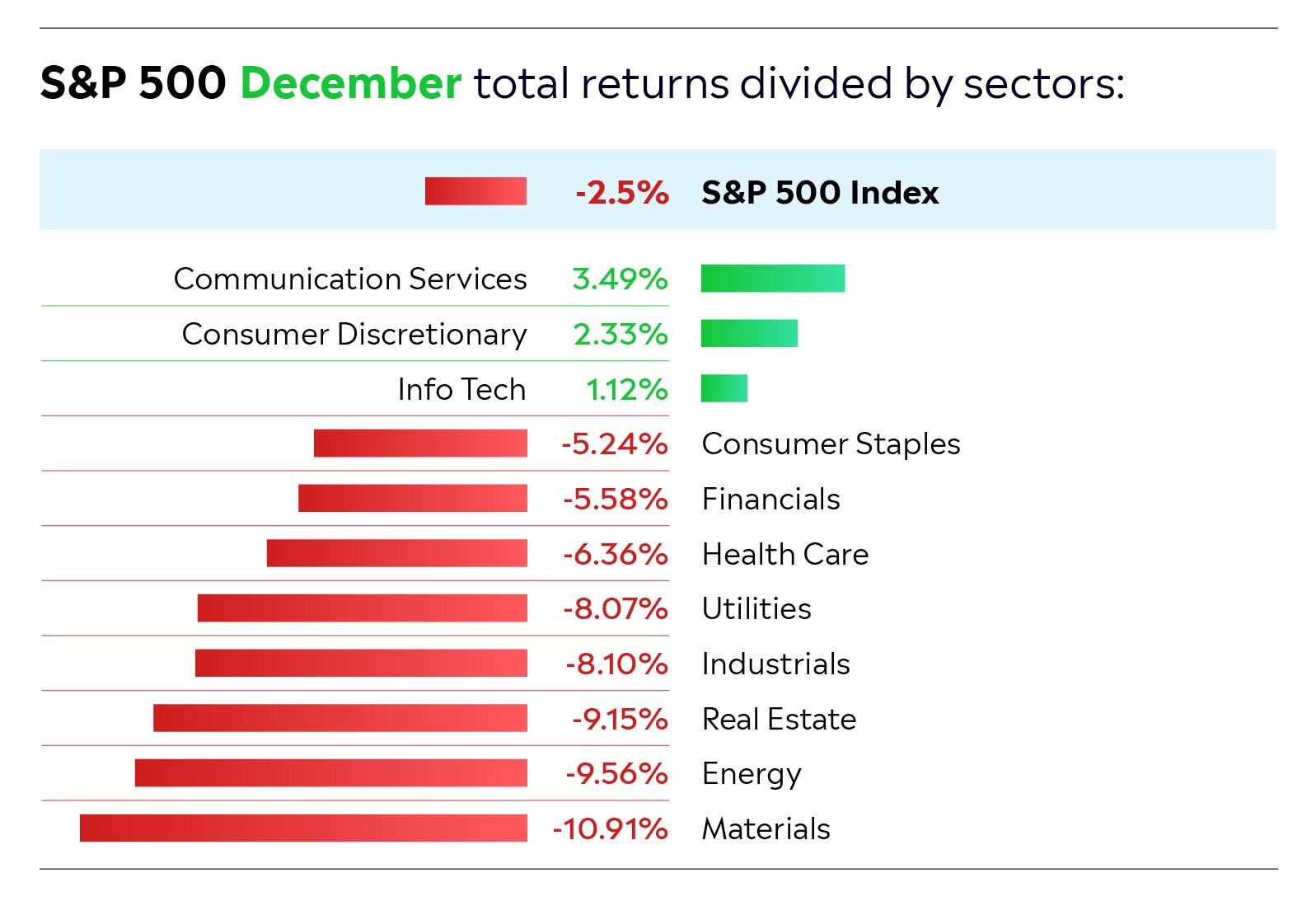

Covering December Market

After November’s strong rally, stocks gave back some of their gains in December amid concerns over rising bond yields and high valuations across the market.

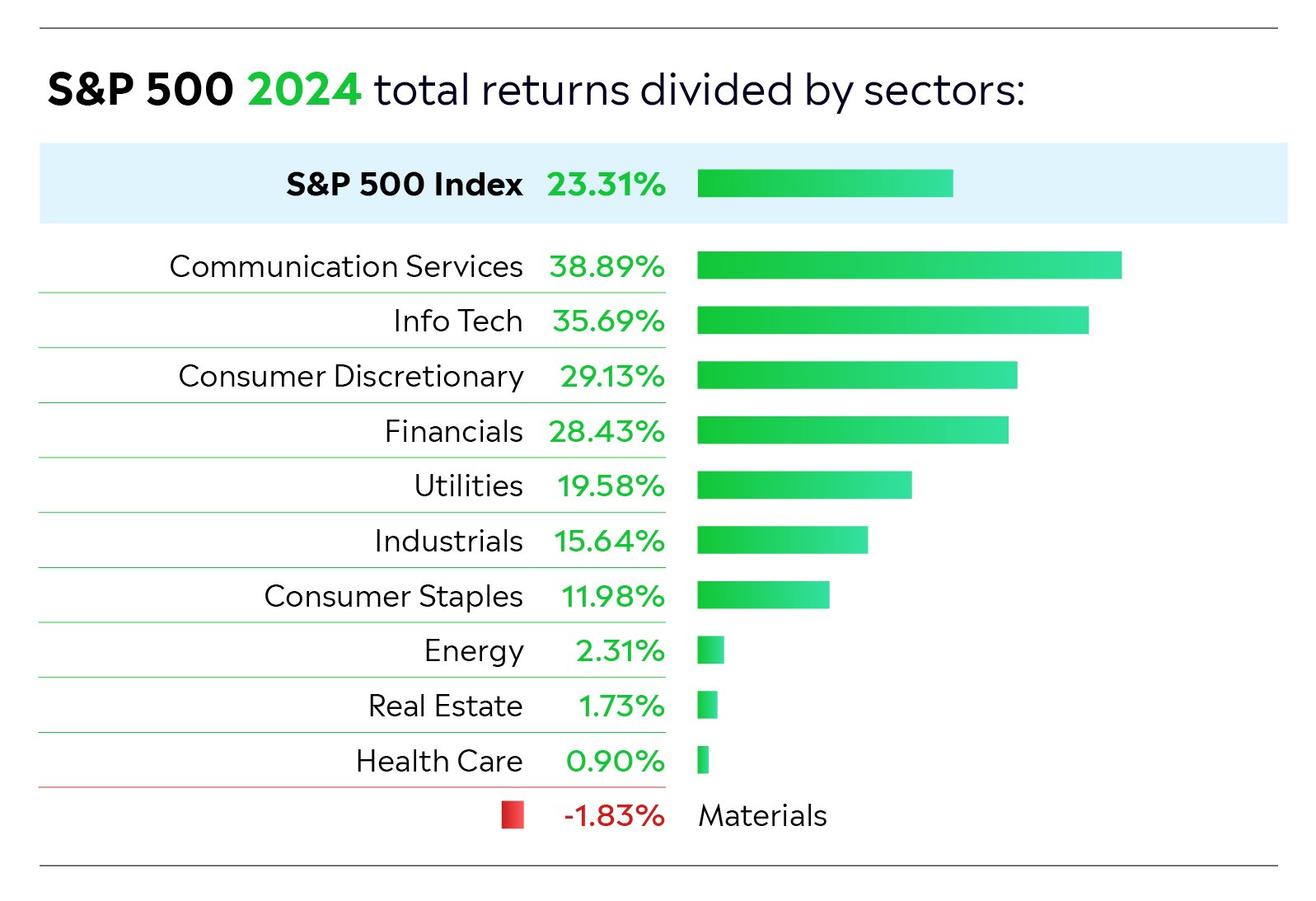

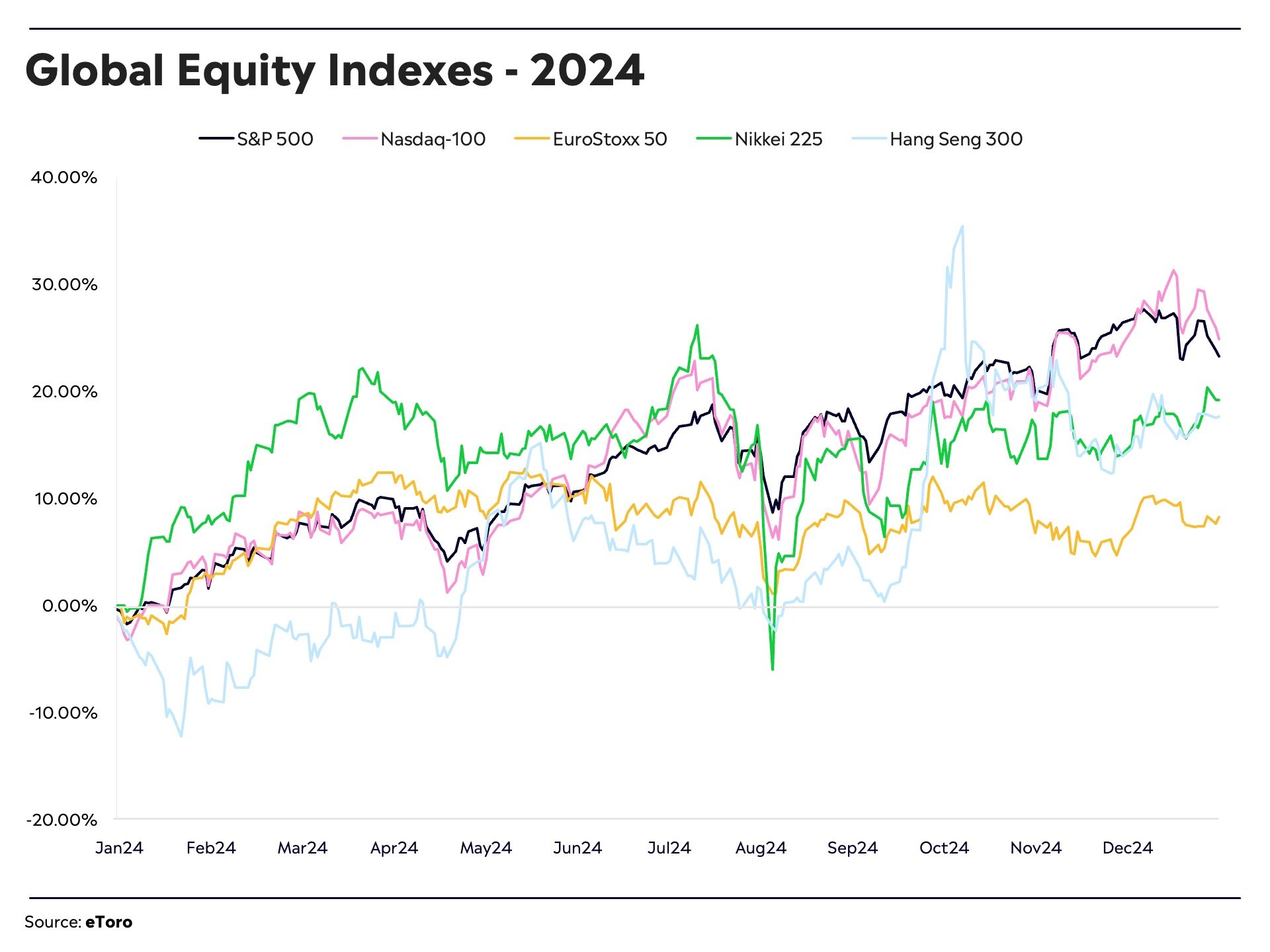

However, 2024 was a very strong year for equities, with the S&P 500 and Nasdaq Indexes delivering returns of 23.31% and 24.88% respectively. European shares produced a lower return of 8.28% as a result of political instability and uncertainty in relation to potential US tariffs in 2025. Yet, Chinese stocks generated double-digit returns despite ongoing economic weakness in China. For the year, the best-performing sectors were Technology, Communication Services, Financials, and Consumer Discretionary. Real Estate, Energy, and Materials were the biggest underperformers.

Artificial intelligence (AI) — the hottest investment theme of 2023 and 2024 — continued to dominate headlines in December (helping to push the Nasdaq above 20,000 for the first time ever).

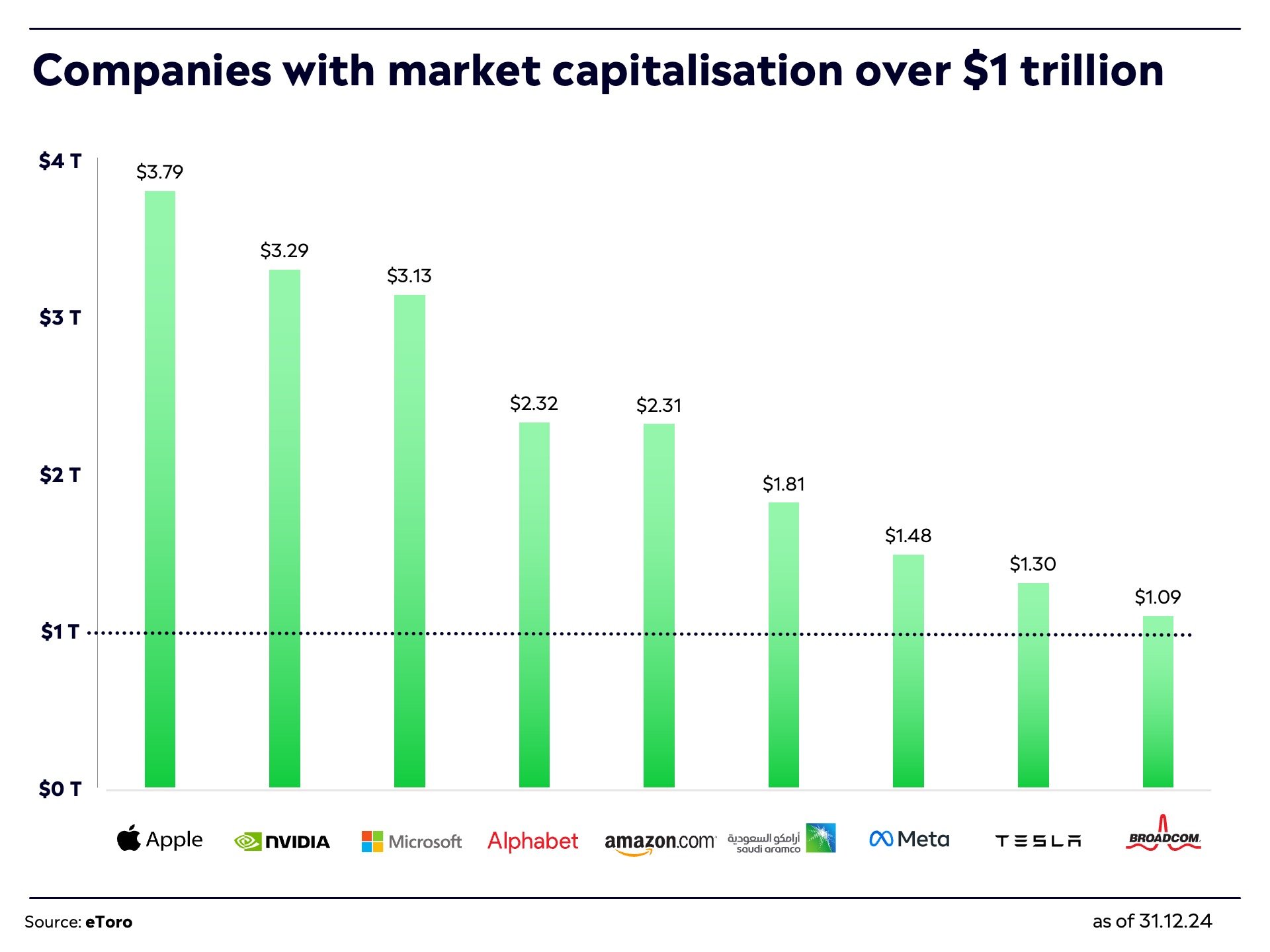

One company that was in the limelight here was Broadcom, which designs custom AI chips for hyperscalers and also offers networking solutions. On its Q4 earnings call, CEO Hock Tan said that AI chips could be a $60–$90 billion opportunity for the company by 2027. This bullish outlook sent the company’s share price up spectacularly and led to Broadcom joining the exclusive trillion-dollar market cap club.

Also in the spotlight was software company Salesforce, which delivered solid fiscal Q3 revenue and earnings growth and raised its Q4 guidance. On its earnings call, CEO Marc Benioff boasted about Salesforce’s “Agentforce” AI agents, which can personalise customer interactions, automate tasks, and improve overall productivity for businesses. Amazon was another company that announced some big developments on the AI front during the month. At its AWS re:Invent conference, it unveiled its “Amazon Nova” foundational models along with its new Trainium3 AI chips.

Picture Credits: Google

Quantum computing was also a hot theme in December.

This form of computing involves using the principles of quantum mechanics to perform computations that are beyond the reach of traditional computers. One company that announced some major news here was Google owner Alphabet. It unveiled a new chip called “Willow,” which only takes five minutes to solve a problem that would currently take the world’s fastest supercomputers ten septillion years to complete (or 1 followed by 25 zeros — years). On the back of this development, and news that Amazon has launched a new program to help enterprises get ready for quantum computing, many smaller quantum computing stocks surged.

Zooming in on the “Magnificent Seven,” performance was mixed in December.

The best performer was Tesla, which gained 17% on the back of excitement over the prospects for the company now that CEO Elon Musk is going to be working closely with Donald Trump to boost government efficiency. Tesla has some exciting automotive technology, however, other car companies are also not standing still. During the month, it came to light that Japan’s Honda and Nissan are exploring a merger. If this deal (which might involve Mitsubishi Motors) was to go through, it would lead to the world’s number three automaker (selling more than 8 million vehicles globally per year). It’s worth pointing out these companies are active in the electric vehicle space, and together, they may be able to better compete against rapidly expanding Chinese automakers.

One theme that underperformed in December was weight-loss drugs.

Here, shares in Danish pharmaceutical powerhouse Novo Nordisk fell sharply after the company published slightly disappointing results for its new drug “CagriSema.” Investors were hoping that this drug — which puts semaglutide (the ingredient in Ozempic and Wegovy) together with a medicine called cagrilintide — would lead to 25% weight loss, however, trials showed only weight loss of 22.7%.

Eli Lilly’s shares rose after the US Food and Drug Administration (FDA) approved the company’s weight-loss drug Zepbound for sleep apnea, yet they still finished the month in negative territory.

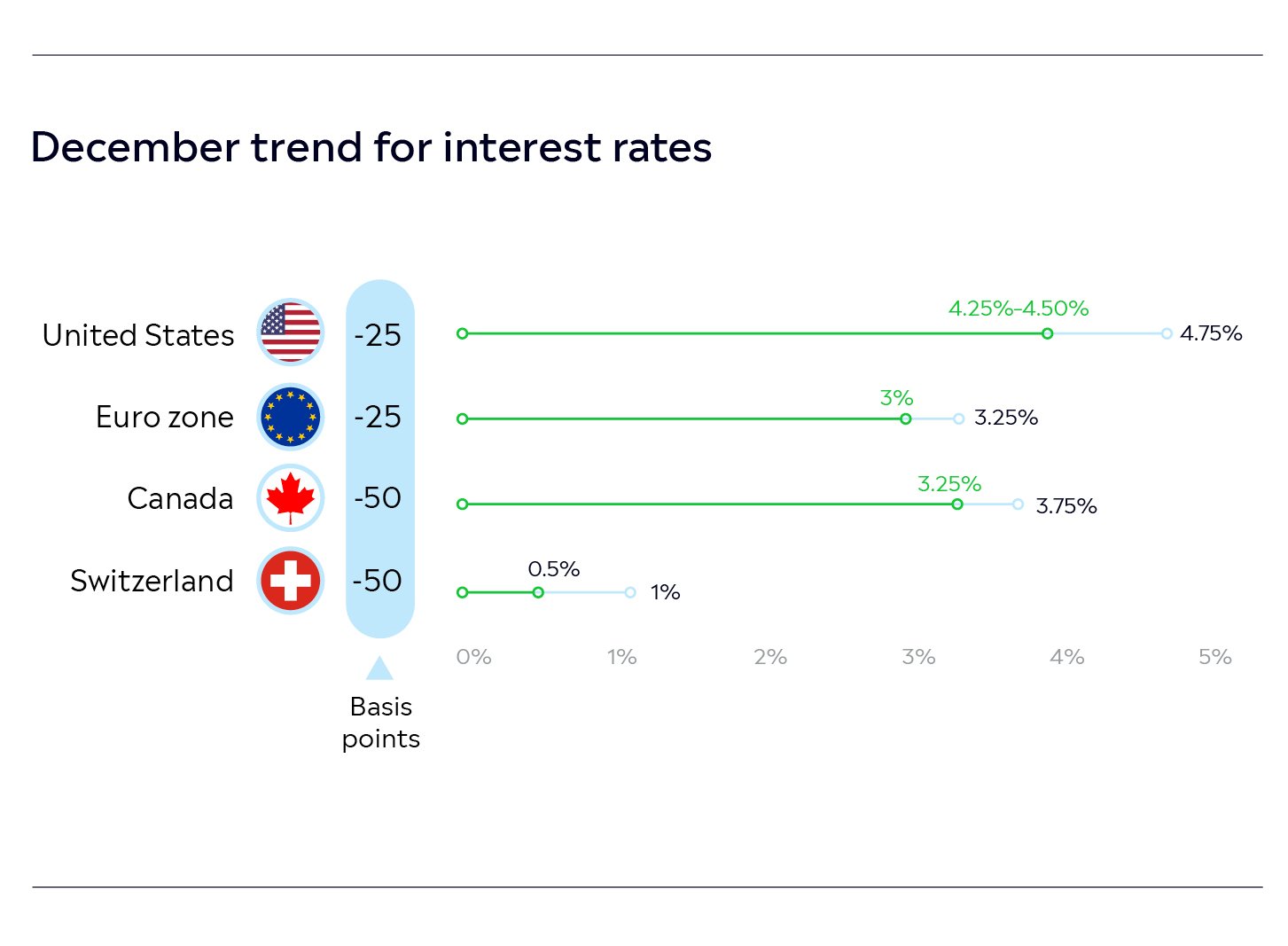

There was a lot of action on the interest rate front in December.

Generally, the trend for rates was down, however, there were some exceptions. As most investors were expecting, the US Federal Reserve made its third cut for the year, reducing rates by 25 basis points to a range of 4.25%–4.50%. However, stocks fell after Fed Chair Jerome Powell advised that going forward, the pace of cuts may be slower than anticipated. Powell was optimistic about the US economy in 2025 and noted that the Fed will need time to assess Trump’s tariffs.

In Europe, the European Central Bank (ECB) made its fourth cut for the year, taking rates down 25 basis points to 3.00%. It kept the door open to more easing — given the high level of political instability across Europe right now (France, Spain, and Germany are all facing political turmoil) and the threat of a fresh US trade war.

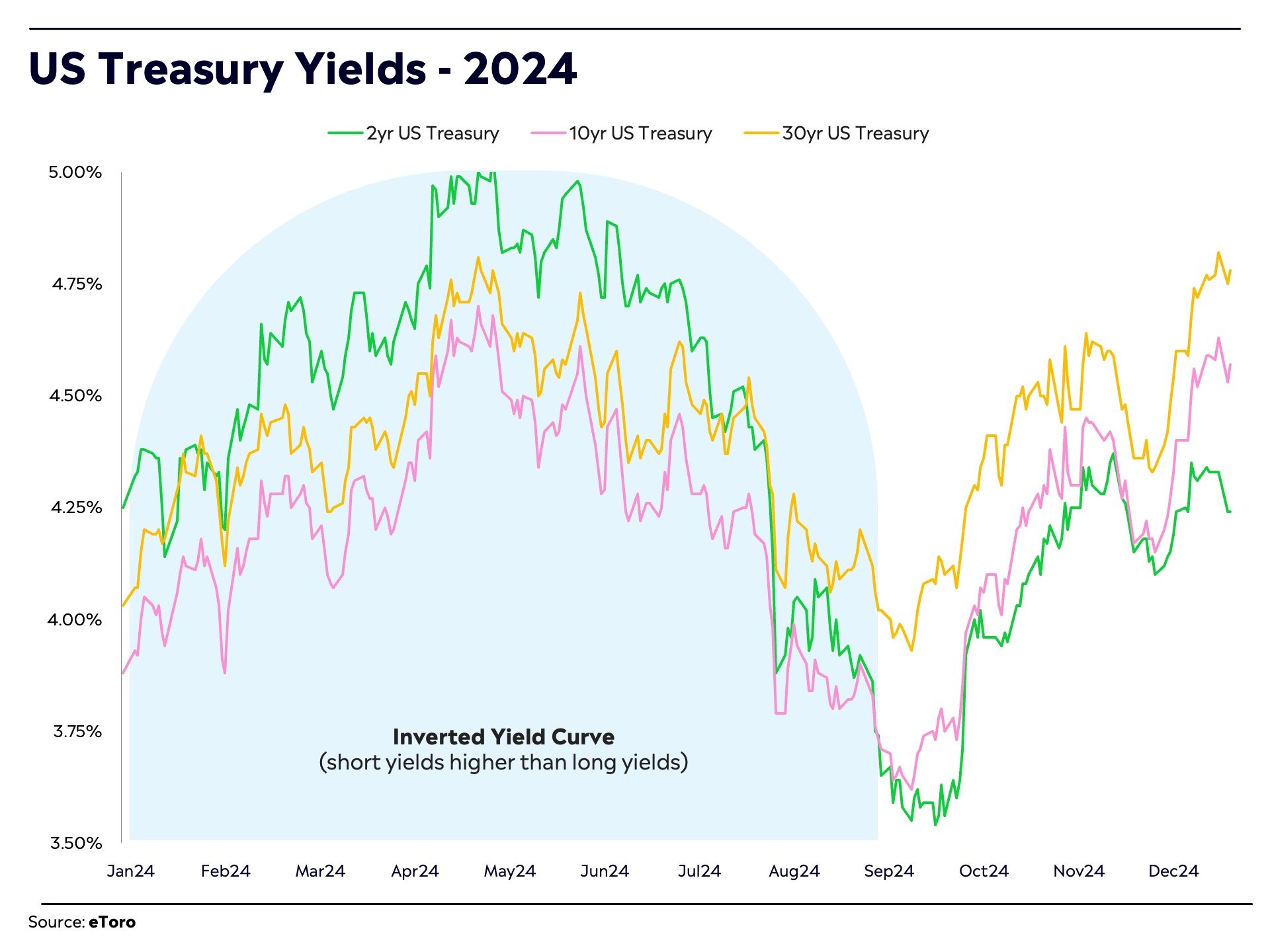

Elsewhere, the Bank of Canada cut rates by 50 basis points to 3.25% while the Swiss National Bank also cut rates by 50 basis points — the biggest reduction in nearly a decade — from 1.0% to 0.5%. Going against the trend was the Central Bank of Brazil, which raised rates by 1% and has planned another two 1% rate hikes for its next meetings. In 2024, the Brazilian real was one of the worst-performing currencies, falling around 21.8% against the US dollar. In terms of government bond yields, the 10-year US Treasury yield ended 2024 above 4.55%, not far off the highest levels of the year. Many analysts believe that a 10-year yield above 5% could put pressure on stocks.

In China, reports claimed that the government is planning to issue 3 trillion yuan ($411 billion) worth of special treasury bonds in 2025 in an effort to stimulate the economy. The proceeds of these bonds will be used to boost consumption via subsidy programs, fund investments in innovation-driven sectors, and upgrade business equipment. Chinese leaders plan to set an annual growth goal of 5% for 2025 and raise the budget deficit to 4% of GDP. However, analysts at Goldman Sachs forecast that China's real GDP growth will slow to 4.5% in 2025 from 4.9% in 2024 due to pressure from US tariffs.

On the commodity front, gold had a relatively flat month. However, it had an excellent year, rising more than 27%. In contrast, oil had a strong month, rising nearly 5%, but was relatively flat for the year. During the month, the price of coffee hit a 50-year high on the back of droughts in Brazil (a major producer). For the year, it produced a gain of around 70%. Cocoa did even better, rising around 180% for the year due to supply constraints.

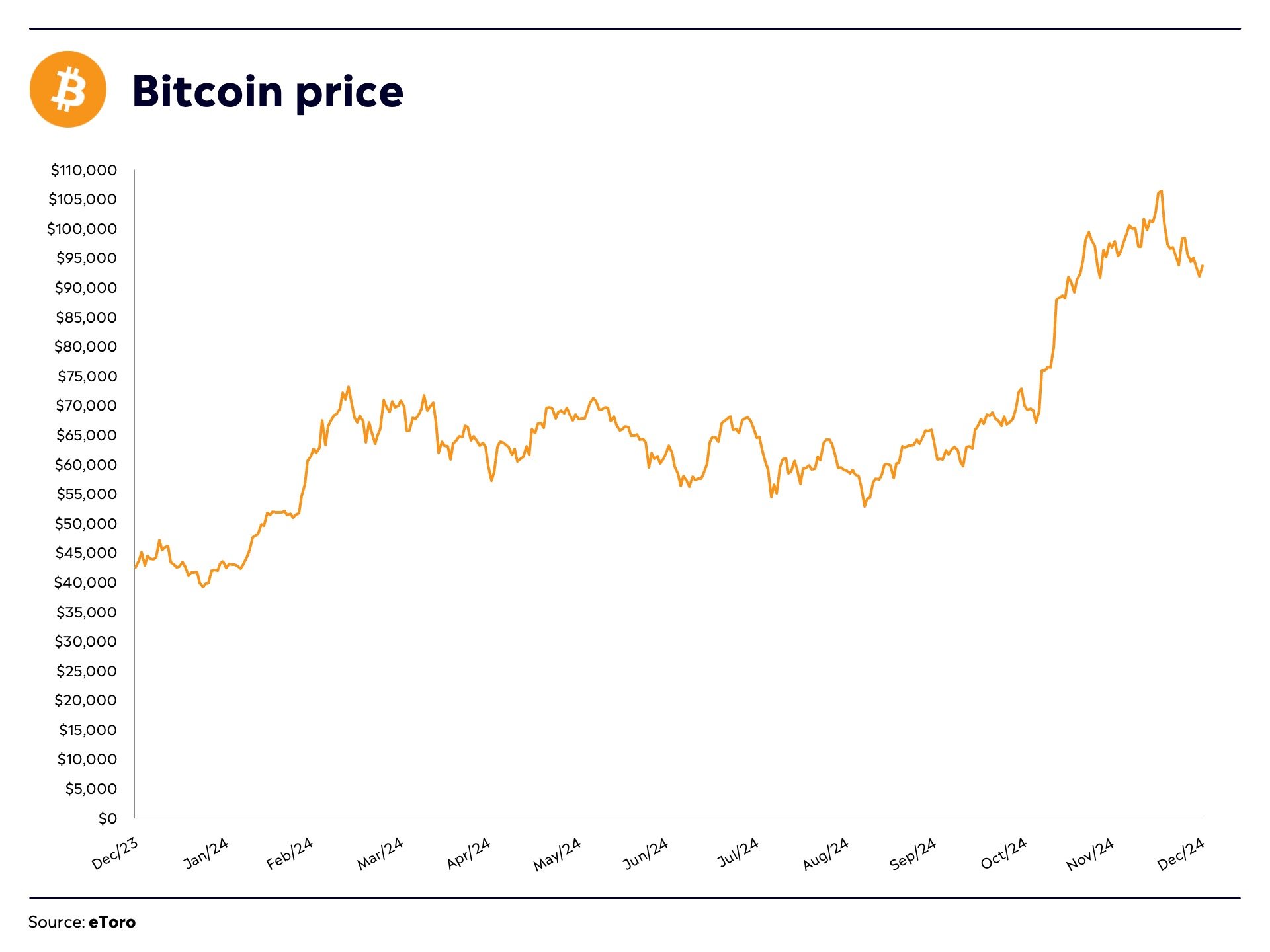

Finally, it was a turbulent month for crypto.

After starting December near $97,000, Bitcoin broke through the $100,000 barrier for the first time ever, soaring all the way to $108,000 (and a $2 trillion market cap). However, the world’s largest cryptoasset then saw some profit taking, pulling back the coin’s value to around $93,500. For the year, Bitcoin produced a gain of 120%, making crypto one of the best-performing asset classes again. Other major cryptoassets including Ethereum, Solana, and Cardano also lost ground in December, but produced strong gains for the year.

BlackRock has recommended that its investors allocate up to 2% in Bitcoin

It’s worth noting that BlackRock, the world’s largest asset manager with over $11 trillion in assets under management (AUM), has recommended that its investors allocate up to 2% of their portfolios to Bitcoin. The investment company has cautioned against exceeding the 2% allocation threshold though, stating that Bitcoin’s contribution to portfolio risk would become disproportionately large beyond this level. Late in the month, BlackRock’s Bitcoin ETF reached $50 billion in assets under management. This product was launched in January 2024 together with other Bitcoin ETFs approved by the US Securities and Exchange Commission (SEC).

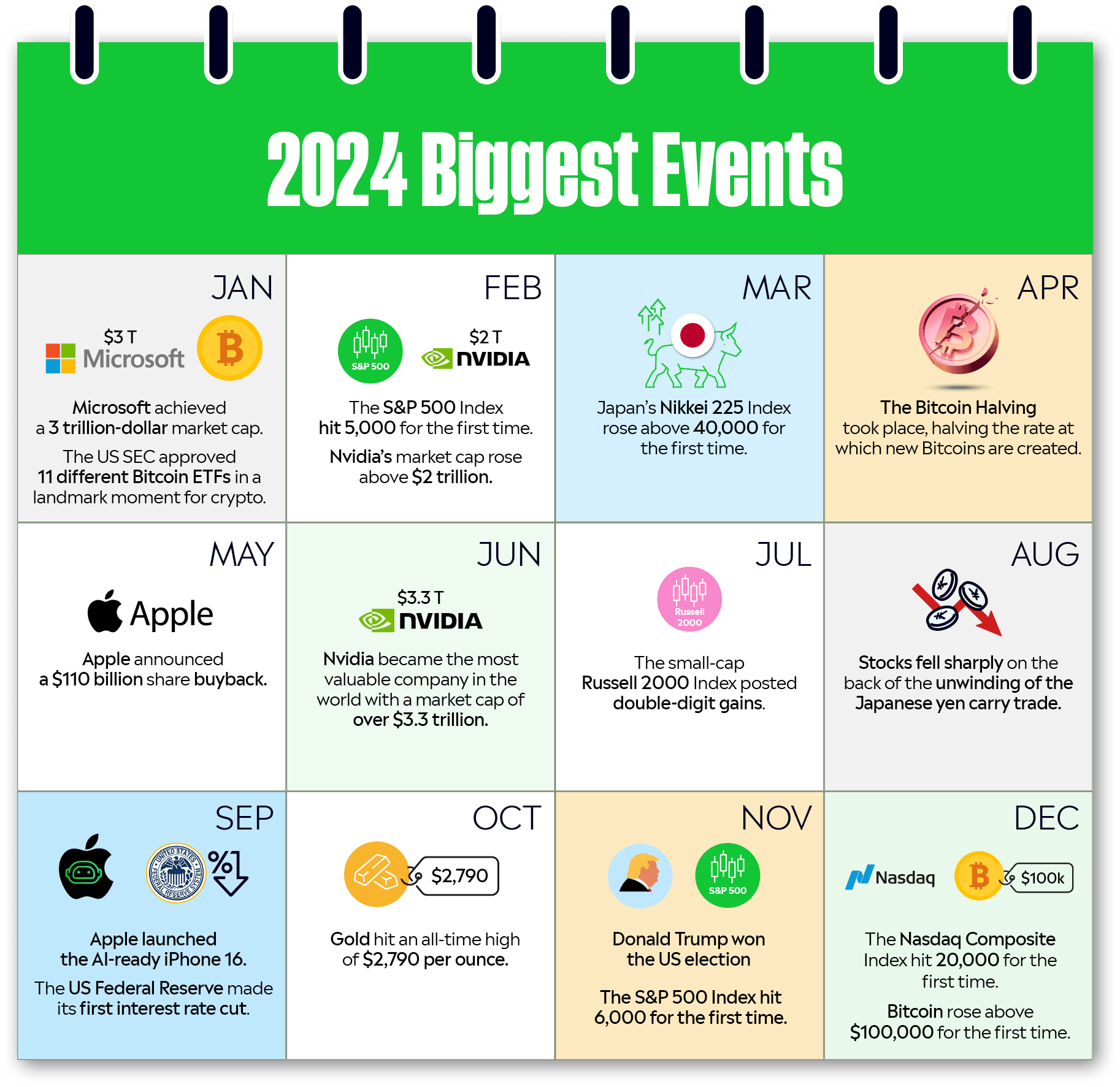

Apple released its Vision Pro headset.

Microsoft achieved a 3 trillion-dollar market cap.

The US SEC approved 11 different Bitcoin ETFs in a landmark moment for crypto.

The S&P 500 Index hit 5,000 for the first time.

Nvidia’s market cap rose above $2 trillion.

Bitcoin hit $50,000 for the first time since 2021.

Reddit listed on the New York Stock Exchange at a valuation of $6.4 billion.

Japan’s Nikkei 225 Index rose above 40,000 for the first time.

Stocks experienced some volatility as bond yields rose and investors worried that interest rates could be higher for longer.

Alphabet announced its first ever dividend.

The Bitcoin Halving took place, halving the rate at which new Bitcoins are created.

Apple announced a $110 billion share buyback — the largest buyback in history.

Nvidia’s CEO Jensen Huang announced that “the next industrial revolution has begun.”

Utilities started to gain traction as a result of the global data centre build out.

The SEC approved the launch of Ethereum ETFs.

Nvidia became the most valuable company in the world with a market cap of over $3.3 trillion.

Apple surged to new all-time highs after it announced the launch of “Apple Intelligence.”

The European Central Bank (ECB) cut interest rates by 0.25% to stand at 3.75%.

Investors rotated out of Big Tech and artificial intelligence (AI) stocks into smaller companies.

The small-cap Russell 2000 Index posted double-digit gains.

Cybersecurity stock CrowdStrike took a hit after the company was responsible for a major IT outage.

Stocks fell sharply on the back of the unwinding of the Japanese yen carry trade.

After a period of volatility, stocks experienced a V-shaped recovery.

Intel’s share price fell 26% in a day — its worst one-day performance since 1974.

Apple launched the AI-ready iPhone 16.

Oil had a weak month, falling to $66 dollar per barrel — the lowest level of the year.

The US Federal Reserve made its first interest rate cut, lowering rates by 0.50% to 4.75%–5.00%.

Conflict in the Middle East rocked stocks early in the month.

Gold hit an all-time high of $2,790 per ounce.

Tesla held its long-awaited robotaxi event, and unveiled several different robotaxi prototypes.

Donald Trump won the US election, sending US stocks up sharply and Bitcoin as high as $99,000.

The S&P 500 Index hit 6,000 for the first time.

Quantum computing stocks surged after Big Tech companies announced that they were getting active in the space.

The Nasdaq Composite Index hit 20,000 for the first time.

Bitcoin rose above $100,000 for the first time.